The stock market closed last week on a positive note, with all three major indexes moving higher. The S&P 500 (SPY) gained about 0.96%, the Dow Jones Industrial Average (DIA) rose 0.79%, and the tech-heavy Nasdaq (QQQ) led with a 2.16% advance.

The Federal Reserve delivered its first rate cut of the year, trimming its benchmark by 25 basis points. That move gave investors confidence that the central bank is ready to support growth after months of elevated inflation and slower economic data. Inflation reports during the week reflected a mixed picture, with consumer prices rising in August while wholesale prices softened, suggesting the Fed may be closer to balancing its efforts between curbing inflation and keeping momentum in the economy.

Looking ahead to the week, markets will be closely watching any additional comments from the Federal Reserve that could hint at the pace of further rate cuts. Investors will also be monitoring fresh inflation readings, consumer spending data, and labor market indicators for clues on the strength of the economy.

While the bulk of corporate earnings season has passed, a few notable reports are still trickling in and could sway sentiment at the margin. At the same time, U.S.–China developments remain an important swing factor. With stocks trading near record highs, attention is turning to whether this rally can sustain or if market participants begin to rotate or lock in profits.

📅 Tuesday, Sep 23rd

- Flash Manufacturing PMI: The upcoming Flash Manufacturing PMI is forecast to ease to 51.8 in September from August’s 53.0, which was the strongest reading since May 2022. August’s strength reflected a return to growth in new orders and production expanding at the fastest pace in over three years, raising the stakes for whether those gains can hold.

Pricing pressures were also in focus, as input costs rose at the second-sharpest pace in three years, with tariffs cited as a key factor behind the increase. A pullback to 51.8 would still signal expansion above the 50.0 threshold but point to slower momentum. Market participants will be watching closely to see whether the moderation reflects fading trade-related stock-building or a more durable recovery in manufacturing demand.

- Flash Services PMI: The upcoming Flash Services PMI is forecast to dip to 53.8 in September from August’s 54.5. August’s reading pointed to a solid expansion in the services economy, supported by resilient demand and strong output growth. A pullback to 53.8 would still indicate expansion above the 50.0 threshold but suggest momentum is cooling from the prior month. Market participants will be watching whether new business inflows, which improved in August, can be sustained at these levels or show signs of slowing. Pricing trends will also be closely monitored, as service providers recently reported elevated cost pressures that could affect inflation expectations and future policy moves.

- Fed Chair Powell Speaks: Fed Chair Jerome Powell is scheduled to speak this week, and markets will parse his remarks for signals on the policy outlook following the recent 25 basis point rate cut that lowered the federal funds target range to 4.00–4.25 percent.

Investors will be listening for any hints on whether further cuts are likely in 2025 or if the Fed intends to pause to assess the impact of easing. Powell’s tone on inflation will be key, as consumer prices are still running above the 2 percent target, with the latest CPI showing annual growth of around 2.9 percent. Traders will also watch how he frames the labor market, which has cooled from last year but remains historically tight. Any shift in emphasis between inflation risks and growth concerns could shape expectations for the path of rates and drive near-term moves in the markets.

📅 Thursday, Sep 25th

- Final GDP q/q: The upcoming Final U.S. GDP report is expected to confirm 3.3% quarter-over-quarter annualized growth, consistent with the prior estimate. The previous reading showed consumer spending rising 1.6%, an improvement from 0.5% in the first quarter, but still moderate. If confirmed, a 3.3% gain would highlight that the economy is expanding at a steady pace despite tighter financial conditions. Market participants will pay close attention to any revisions in consumer spending and business investment, the latter of which was revised higher in the last estimate.

- Unemployment Claims: The next U.S. Unemployment Claims report is expected to show around 235,000 initial claims, compared with the prior week’s 231,000. A modest increase would point to a labor market that is gradually cooling, though claims remain relatively low compared with historical norms.

Market participants will also watch continuing claims, which stood at about 1.92 million in the latest report, since an upward move could indicate it is taking longer for workers to find jobs. The data will be assessed in the context of the Federal Reserve’s effort to balance moderating inflation with maintaining employment. The results will help shape perceptions of how quickly labor market conditions are easing and what that could mean for policy in the months ahead.

📅 Friday, Sep 26th

- Core PCE Price Index m/m: The upcoming Core PCE Price Index report is forecast to show 0.2% month-over-month growth for August, down from the prior reading of 0.3%. This measure is closely watched by the Federal Reserve as its preferred gauge of underlying inflation, excluding food and energy. A softer print at 0.2% would suggest that inflation pressures are easing gradually toward the Fed’s 2% target. Market participants will monitor whether services inflation, which has been sticky in recent months, shows signs of cooling. The data could influence expectations for the pace of future rate cuts and shape market sentiment across equities, bonds, and the dollar.

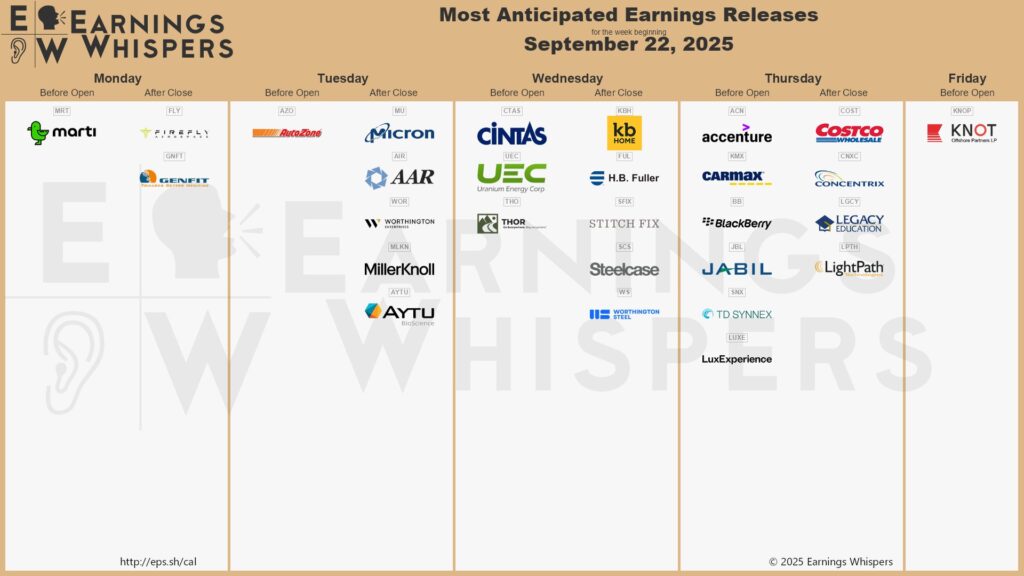

💼 While most of earnings season is behind us, a handful of well-known companies are still set to announce results this week.

📅 Tuesday, Sep 23rd

- Micron Technology, Inc. (MU): Micron is set to report fiscal Q4 earnings, with Wall Street closely watching whether the company can deliver on its recently raised guidance. The company now expects revenue of $11.2 billion ± $100 million, compared with a prior forecast of $10.7 billion ± $300 million, and adjusted earnings per share of $2.85 ± $0.07, up from $2.50 ± $0.15.

Gross margins are anticipated at 44.5% ± 0.5%, an improvement attributed by Micron to stronger pricing, particularly in DRAM, and solid execution. Market participants will be watching closely to see if actual results meet these higher targets and how management frames its outlook for fiscal Q1. Commentary on demand trends, product mix, and long-term investment plans will be key in shaping market reaction after the release.

- AutoZone, Inc. (AZO): AutoZone is expected to report Q4 revenue of approximately $6.24–$6.25 billion, compared to about $6.21 billion in the prior-year quarter, which included an extra (17th) week. Earnings per share are forecast in the range of $50.7–$51.1, slightly below the $51.58 EPS reported in the year-ago quarter.

Key areas to watch include U.S. same-store sales growth, which rose 5.0% last quarter and will signal whether momentum is holding as comparisons toughen. International performance in Mexico and Brazil has been strong on a constant-currency basis, but FX translation remains a drag. Margin pressure from freight, import costs, and wages will also be in focus, especially given recent gross margin declines tied to these factors. Market participants are also monitoring the company’s store and mega-hub expansion strategy and how management frames priorities for fiscal 2026, given AutoZone’s practice of not issuing formal numerical guidance.

📅 Wednesday, Sep 24th

- Cintas Corporation (CTAS): Cintas is preparing to release its fiscal Q1 2026 earnings, with analysts expecting revenue of about $2.70 billion, an 8% increase from last year, and earnings per share of $1.19, which would reflect an 8.1% growth. Market participants will be watching closely to see if the company can maintain its recent record operating margins of 22.4 to 22.8 percent, which were achieved in the previous quarter as cost control and pricing discipline boosted profitability.

The company has guided for full-year revenue of $11.0 to $11.15 billion and EPS of $4.71 to $4.85, making this report an important test of whether those targets remain realistic. Segment performance will be a focal point as well, with Uniform Rental and Facility Services continuing to anchor the business and First Aid and Safety Services showing stronger growth potential, while traders will also look for management’s commentary on labor expenses, input costs, foreign currency movements, and tax rate impacts, all of which could play a role in shaping results over the rest of the year.

📅 Thursday, Sep 25th

- Costco Wholesale Corporation (COST): Costco is set to report its Q4 fiscal 2025 results, with analysts expecting earnings per share of about $5.80–$5.81, compared with $5.29 in the same quarter last year. In the prior quarter, Costco posted $63.2 billion in total revenue, including $61.97 billion in net sales, both up roughly 8% year over year, underscoring the high bar for growth heading into this report.

Market participants will be watching closely for trends in comparable sales across the U.S. and international markets, as well as membership fee income and renewal rates, which remain central to Costco’s profitability. Other areas of focus include inventory management, the impact of tariffs and supply-chain pressures, and margin performance in the face of rising costs. Although Costco does not issue formal forward guidance, investors will parse management’s commentary on business conditions and the impact of its September 2024 membership fee increase to help shape expectations for the upcoming fiscal year.

- Accenture plc (ACN): Accenture is scheduled to report its fourth quarter fiscal 2025 results, following a strong Q3 where revenue came in at $17.7 billion, up 7.6% year-over-year, and EPS rose to $3.49, up 11.5% from the prior year. Analysts expect Q4 revenue in the range of $17.0 billion to $17.6 billion, with full-year revenue growth in local currency estimated at 6–7%. Key indicators to watch include new bookings (especially how consulting-versus-managed services mix evolves), operating margin trends (will margin expansion continue after the 40 basis point gain in Q3 to ~16.8%), and how demand for GenAI / digital transformation is contributing to both bookings and revenue.

Market participants will also be looking for guidance on federal business exposure (which was flagged as a headwind), FX / foreign currency impacts, and cash flow / capital return metrics (share buybacks, dividends) to gauge how Accenture intends to balance growth with margin pressure and rising investment in emerging technologies.

We hope this helps and happy trading!

– Trade and Travel Team

Related Blogs

Follow Us

Testimonials

Hear from students on why they chose the Trade and Travel Family and how it has changed their lives.