A cautious tilt marked last week’s trading as investors digested a fresh wave of corporate earnings, Federal Reserve commentary, and economic data ahead of September’s key reports. The S&P 500’s SPY ETF was essentially flat for the week. In contrast, the Nasdaq-100’s QQQ slipped about 0.27% and the Dow Jones Industrial Average, tracked by the DIA ETF, declined roughly 0.12%.

Earnings season remains a key reason behind equity moves. Although the pace of reports has slowed, last week featured a mix of beats and cautious outlooks that reinforced the broader narrative: companies are generally surpassing near-term estimates even as they temper guidance for the year ahead. That underlying strength helped indices hover near record levels.

The most market-moving event, however, came from Jackson Hole, where Fed Chair Jerome Powell signaled a growing consensus for a September rate cut. His remarks on a “shifting balance of risks” boosted confidence that the central bank will begin easing monetary policy. Fellow policymakers echoed his tone, with several officials indicating support for a quarter-point reduction in borrowing costs once retail sales and inflation readings confirm a persistent cooling trend.

As markets look toward the holiday-shortened week, the August jobs report due September 5th will command the spotlight. Consensus forecasts call for payroll growth below 100,000, a figure that could cement the Fed’s case for easing or, if surprisingly strong, force a recalibration of expectations. Alongside employment data, traders will monitor PMI readings, job openings, and a lighter slate of earnings from companies like Broadcom and Salesforce. With volatility subdued and indices near highs, last week’s muted moves set the stage for what promises to be a data-driven September.

📅 Monday, Sep 1st

- Happy Labor Day! (Markets are closed)

📅 Tuesday, Sep 2nd

- ISM Manufacturing PMI: The upcoming report will be closely watched as economists forecast an improvement to 48.9 from the previous reading of 48.0 in July. While this represents the fifth consecutive month the index would remain below the critical 50.0 expansion threshold, indicating continued manufacturing contraction, the expected 0.9-point increase suggests the pace of decline may be moderating.

Market participants should focus on key subcomponents, including new orders (previously at 47.1), employment (which dropped to a concerning 43.4 in July), and production (the bright spot at 51.4), as these metrics will signal whether the manufacturing sector is stabilizing or heading toward further weakness. Additionally, any reading above the 48.9 forecast could spark risk-on sentiment and strengthen the dollar, while a miss below expectations may reinforce concerns about manufacturing resilience and prompt dovish Federal Reserve speculation.

📅 Wednesday, Sep 3rd

- JOLTS Job Openings: The upcoming report is expected to show 7.24 million job openings, representing a 200,000 decline from June’s 7.44 million level. This anticipated decrease would continue the steady cooling trend in labor demand since the 12 million peak in 2022, with markets closely watching whether openings fall toward the critical 7 million threshold that could trigger Federal Reserve rate cut expectations.

Market participants should monitor key dynamics including the job openings-to-unemployed worker ratio (currently around 1.06, per June JOLTS data), quits rates as a measure of worker confidence, and regional distribution changes, as any significant deviation from the 7.24 million forecast could influence Fed monetary policy decisions, particularly with markets pricing approximately 85–86% probability of a 25-basis-point rate cut in upcoming meetings if labor conditions deteriorate markedly.

📅 Thursday, Sep 4th

- ADP Non-Farm Employment Change: The upcoming report is expected to show private sector job additions of 71,000 for August 2025, marking a significant slowdown from July’s actual figure of 104,000 jobs. This forecasted decline of approximately 32% month-over-month represents a concerning deceleration in private sector hiring momentum, as the labor market continues to show signs of cooling amid economic uncertainties and the lingering effects of trade policy adjustments. Market participants should closely monitor whether the actual figure aligns with, exceeds, or falls short of the 71,000 consensus estimate, as significant deviations could trigger heightened market volatility and influence Federal Reserve policy expectations.

- Unemployment Claims: The upcoming report is expected to show initial claims remaining steady at 229K, matching both the previous week’s reading and consensus forecasts, signaling continued labor market stability amid broader economic uncertainty. With the 4-week moving average currently at 228.5K and continuing claims holding at 1.954M, investors should monitor whether the data stays within the 225K-235K range that has characterized recent weeks, as any significant deviation could signal either strengthening or weakening labor market conditions. Traders should pay particular attention to Federal Reserve policy implications, as Governor Waller recently indicated that labor market data will be crucial for September’s anticipated 25 basis point rate cut decision, making any surprise in the claims numbers potentially market-moving for both equities and the US Dollar.

- ISM Services PMI: The August ISM Services PMI is forecast at 50.5, up from July’s 50.1, indicating a slight acceleration in service-sector activity above the neutral 50 threshold. A print above 50.5 would confirm broadening expansion and could support risk assets. Market participants should monitor subindexes carefully. New Orders were 50.3 in July, signaling revenue trends. By contrast, Employment was in contraction at 46.4, and Backlog of Orders remained weak at 44.3. Notably, Prices Paid registered a high 69.9, indicating persistent input-cost pressures.

📅 Friday, Sep 5th

- Average Hourly Earnings m/m: August’s Average Hourly Earnings are expected to rise by 0.3% month-over-month following July’s 0.3% gain. Investors should watch whether the actual figure beats or misses the 0.3% forecast, as a stronger print could signal renewed wage-driven inflation pressure and bolster interest-rate expectations. Market participants will also monitor revisions to prior months and the reaction in Treasury yields and equity volatility for clues on Federal Reserve policy direction.

- Non-Farm Employment Change: The U.S. Non-Farm Employment Change report is due to be released with a consensus forecast of 74,000 jobs added in August, up slightly from the prior month’s 73,000 gain. Market participants should focus on the breakdown between goods-producing and service-sector employment to gauge whether manufacturing or services are driving the labor market’s resilience. Traders will be watching average hourly earnings and the unemployment rate reaction closely, as any upside surprise could intensify expectations for tighter monetary policy.

- Unemployment Rate: The upcoming US unemployment rate report is forecast at 4.3%, up from last month’s 4.2%. Labor force participation, currently at about 62%, will reveal whether more workers are entering or exiting the job market. Market participants will monitor whether the actual rate deviates from 4.3% and watch initial jobless claims and labor force participation for signs of underlying labor market momentum.

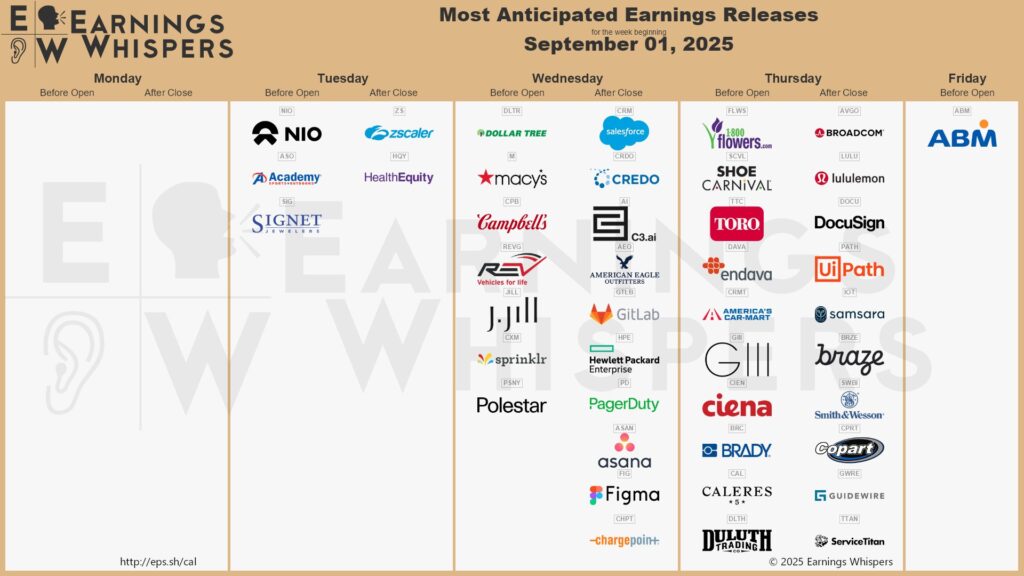

💼 With earnings season wrapping up, here are some of the companies reporting this week:

📅 Wednesday, Sep 3rd

- Macy’s Inc. (M): Macy’s will report its Q2 2025 results with analysts forecasting adjusted earnings per share of $0.19, representing a 64.2% year-over-year decline, on revenue of $4.70 billion, down 4.8% from the year-ago quarter. Market participants should watch for any improvement in comparable sales, which fell 2.0% last quarter across Macy’s, Inc., as well as continued momentum in digital sales, which now account for about one-third of total revenue. Margins remain under pressure: Q1 operating income was just 2.0% of sales (with adjusted EBITDA margin at 6.8%), and traders will be looking for signs of stabilization.

- Salesforce, Inc. (CRM): Salesforce will report Q2 earnings, with analysts forecasting adjusted EPS of $2.78 per share, an 8.5% increase year-over-year. Consensus revenue stands at approximately $10.14 billion. Subscription and support revenue, which reached $9.3 billion in Q1 (+8% year-over-year), will remain the core growth driver. Current remaining performance obligations (CRPO) totaled $29.6 billion in Q1, growing 12% YoY and serving as a key indicator of future revenue. Full-year FY26 guidance was raised to $41.0–$41.3 billion in revenue and $11.27–$11.33 in EPS, a $400 million increase at the high end that underscores confidence in AI investments and the Informatica acquisition.

- Hewlett Packard Enterprise Company (HPE): HPE will release its Q3 results with Wall Street expecting revenue around $8.35 billion and EPS of $0.42, in line with the company’s Q3 guidance of $8.2–$8.5 billion and $0.40–$0.45 EPS. Market participants should closely monitor management comments on AI and hybrid cloud momentum, as HPE reported over $1 billion in AI systems revenue in Q2 and exited the quarter with an AI backlog of $3.2 billion. Hybrid Cloud revenue rose 13% year over year to $1.5 billion. Financial health remains under scrutiny: Q2 saw a negative free cash flow of $847 million, though management reaffirmed its full-year free cash flow target of about $1 billion. Analysts will also look for updates to full-year 2025 guidance, which currently stands at 7–9% constant currency revenue growth and $1.78–$1.90 EPS.

📅 Thursday, Sep 4th

- Broadcom Inc. (AVGO): Broadcom will report third-quarter fiscal 2025 results, with analysts projecting earnings per share of $1.66 on revenue of $15.8 billion, up 33.8% and 21.1% year-over-year, respectively. Market participants should focus on management’s guidance for revenue (currently pegged at around $15.8 billion) and Adjusted EBITDA margin, forecast at a minimum of 66% of revenue, as well as the trajectory of AI-driven segment sales, expected to rise from $4.4 billion in Q2 to roughly $5.1 billion next quarter. Additionally, monitoring any revisions to full-year EPS guidance of $5.47 and commentary on enterprise software versus semiconductor end-market demand will be crucial for assessing the sustainability of Broadcom’s growth.

- lululemon athletica inc. (LULU): Lululemon will report Q2 FY2025 with analysts forecasting adjusted EPS of $2.86, a 9.2% year-over-year decline, on revenue of $2.54 billion, up 7.2% year-over-year. A key focus will be same-store sales in the Americas, down 2.0% last quarter, and the pace of digital and international growth, particularly in China and other markets. Finally, traders should monitor SG&A (Selling, General, and Administrative) leverage against top-line growth and elevated inventory levels (up 23% YoY) as indicators of margin resilience or potential markdown risks.

We hope this helps and happy trading!

– Trade and Travel Team

Related Blogs

Follow Us

Testimonials

Hear from students on why they chose the Trade and Travel Family and how it has changed their lives.