Wall Street experienced heightened volatility last week as President Trump’s official announcement of 25% auto tariffs, set to begin on April 2nd, along with reciprocal tariffs, triggered broad sell-offs across global markets.

The SPY (S&P 500) retreated 1.48% for the week. The tech-heavy Nasdaq, QQQ, closed down 2.47% for the week. Meanwhile, the DIA (Dow Jones Industrial Average) managed to limit losses compared to broader indices, declining 0.95%. This marked a sharp reversal after the previous week’s gains when the SPY and QQQ had snapped a four-week losing streak.

Market participants also grappled with a hotter-than-expected inflation report and weakening consumer sentiment. The personal consumption expenditures (PCE) index indicated a 2.8% year-over-year price increase in February, slightly above the 2.7% forecast. Additionally, the University of Michigan’s survey revealed a decline in consumer sentiment, with the index reading at 57, the lowest since late 2022.

Looking ahead, investors and traders should keep an eye on several key events.

📅 Tuesday, April 1st

- ISM Manufacturing PMI: The upcoming ISM Manufacturing PMI report is forecasted at 49.6, which would indicate ongoing contraction in the manufacturing sector. Investors and traders should closely monitor key subcomponents including new orders (previously at 48.6), production (50.7), employment (47.6), and the prices index (62.4) to gauge whether inflationary pressures are continuing to accelerate amid ongoing manufacturing weakness. A reading above 50 would signal an unexpected expansion in manufacturing activity, potentially triggering market volatility, while a reading below 47.0 could intensify concerns about broader economic weakness.

- JOLTS Job Openings: The upcoming JOLTS Job Openings report is forecasted at 7.73 million, slightly below January’s 7.74 million but still reflecting resilience in the labor market despite recent fluctuations. Investors and traders should closely monitor the ratio of job openings to unemployed workers, which stood at 1.13 in January, as this key metric provides critical insight into labor market tightness and potential wage pressures that could influence Federal Reserve policy decisions.

📅 Wednesday, April 2nd

- ADP Non-Farm Employment Change: The upcoming ADP Non-Farm Employment Change report is forecast to show 118,000 private jobs added in March 2025, which would represent a significant 53% increase from February’s disappointing 77,000 figure yet remain below January’s robust 183,000 job additions. Investors should closely monitor sectors that previously showed weakness, particularly trade/transportation/utilities which lost 33,000 jobs and education/health services which shed 28,000 jobs in February. Traders will want to compare the ADP figure with the subsequent BLS Non-Farm Payrolls report to gauge labor market momentum, as recent months have shown discrepancies between the two reports with February’s ADP showing only 77,000 jobs while the BLS reported 151,000 for the same period.

📅 Thursday, April 3rd

- Unemployment Claims: The upcoming initial jobless claims report is forecasted to reach 227K, slightly above the recent 224k moving average, with investors closely monitoring whether this represents normal fluctuation or a potential weakening in the labor market’s resilience. Market participants should pay particular attention to continuing claims, which have been elevated at approximately 1.86 million and have failed to drop below 1.8 million since May 2024, as persistent high levels could signal deteriorating hiring conditions with implications for Federal Reserve policy decisions.

- ISM Services PMI: The upcoming ISM Services PMI report is forecast at 53.0, slightly below February’s reading of 53.5 but still indicating continued expansion in the services sector for what would be the ninth consecutive month. Investors and traders should closely monitor the four key components: Business Activity (previously 54.4), New Orders (previously 52.2), Employment (previously 53.9), and Supplier Deliveries (previously 53.4), with particular attention to the Prices Index which rose to 62.6 in February, signaling persistent inflation pressures. Market participants should also watch for commentary regarding potential tariff impacts and federal spending cuts, as these concerns were highlighted by respondents in previous reports and could influence service sector outlook amid the broader economic environment.

📅 Friday, April 4th

- Average Hourly Earnings m/m: The upcoming Average Hourly Earnings month-over-month report is forecasted to show a 0.3% increase, consistent with the February 2025 figure when wages rose to $35.93 per hour. Investors and traders should closely monitor whether the actual figure deviates from the 0.3% forecast, as higher readings above 0.4% could signal accelerating wage pressures that might concern the Federal Reserve about inflation persistence. Market participants should also compare the year-over-year figure against the previous 4.0% reading, as sustained wage growth above 4.1% could potentially delay anticipated rate cuts.

- Non-Farm Employment Change: The upcoming Non-Farm Employment Change report is forecast to show 139,000 new jobs added to the US economy, signaling a potential continued cooling in the labor market following February’s 151,000 and January’s downwardly revised 125,000 jobs. Investors and traders should pay particular attention to wage growth, currently at 4.0% annually, as well as any revisions to previous months’ figures, which could significantly impact Federal Reserve policy expectations amid growing concerns about economic headwinds from Trump’s tariff plans and federal spending cuts that have already contributed to 10,000 federal government job losses in February.

- Unemployment Rate: The upcoming March unemployment rate report is expected to hold steady at 4.1%, following February’s increase from 4.0% to 4.1% amid modest job growth of 151,000 positions. Recent labor market data show concerning trends, including a declining labor force participation rate of 62.4%. Investors and traders should closely monitor three key indicators: whether monthly job creation maintains the 100,000-150,000 level needed for labor market stability, any shifts in the labor force participation rate that could signal changing workforce dynamics, and potential impacts from trade policy uncertainties that economists warn could undermine employment resilience in coming months.

- Fed Chair Powell Speaks: Investors should closely monitor Federal Reserve Chair Jerome Powell’s assessment of inflation, which remains elevated at 2.5% PCE and 2.8% core PCE as of February, alongside his views on the potential stagflationary impact of recent trade policies.

Traders should pay particular attention to any signals regarding the timing of the upcoming rate cuts for 2025, especially given the central bank’s recent downward revision of GDP growth to 1.7% from 2.1% previously forecasted in December. Market participants should also watch for Powell’s commentary on whether consumer spending continues to moderate and if near-term inflation expectations, which have recently increased due to tariff concerns, might force the Fed to maintain its current 4.25% to 4.5% target range longer than anticipated.

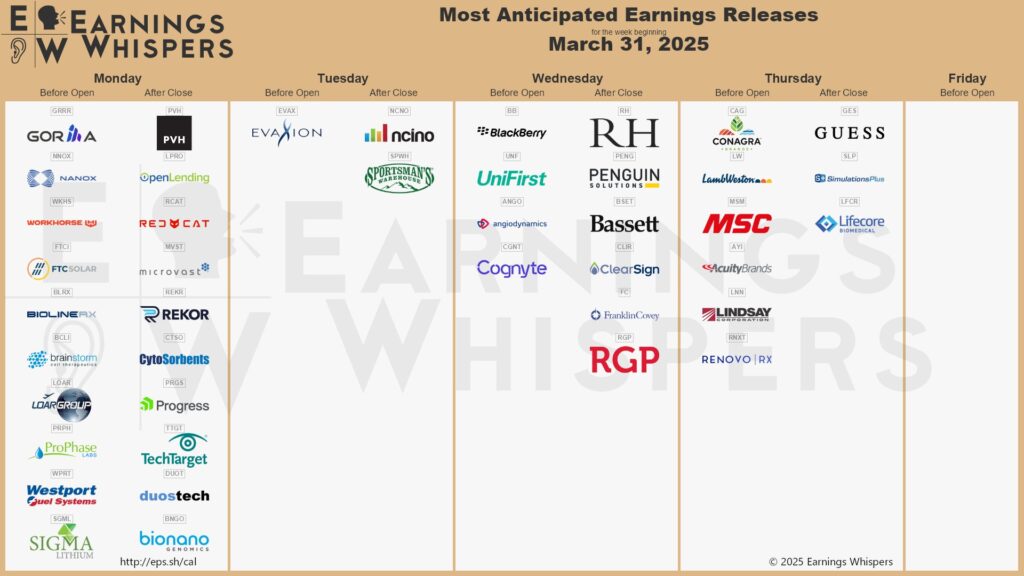

Here are some stocks reporting earnings this week:

📅 Monday, Mar 31st

- PVH Corp (PVH) is set to release its earnings report after market close, with analysts expecting earnings per share (EPS) of $3.21 and revenue of approximately $2.33 billion. Investors should note that these projections represent a concerning year-over-year decline, with revenue expected to decrease by 6.4% compared to the same period last year and EPS potentially falling by 13.7%. Key focus areas for investors and traders should include Calvin Klein and Tommy Hilfiger brand performance, guidance for the upcoming fiscal year, and margin trends as the company navigates challenging retail conditions.

📅 Wednesday, April 2nd

- RH (formerly Restoration Hardware) will report is earnings with investors focused on whether the luxury retailer meets its 18-20% revenue growth target ($871–$885 million) and 12.2–13.2% adjusted operating margin, alongside a consensus EPS estimate of $1.88 (161% YoY surge from Q4 2023’s $0.72). Traders will scrutinize CEO Gary Friedman’s commentary on sustaining November’s 24% demand spike and December’s 30% acceleration, as well as progress in shifting 15–25% of supply chains from China to Mexico to mitigate tariff risks, while managing elevated inventories of $978.6 million.

📅 Thursday, April 3rd

- Conagra Brands (CAG) is scheduled to release its earnings results with analysts expecting quarterly earnings of $0.52 per share, representing a significant year-over-year decline of 24.6%, and revenues of $2.9 billion, down 4.29% from the year-ago quarter. Investors should pay close attention to the impact of previously announced supply constraints, particularly issues affecting frozen meals containing chicken and frozen vegetables, which prompted the company to lower its full-year EPS guidance from $2.45-$2.50 to $2.35 in February. Market participants would also benefit from monitoring management’s comments on inflation pressures, foreign exchange headwinds, and any updates to the company’s organic net sales forecast, which was previously adjusted downward by 2 percent.

We hope this helps and happy trading!

– Trade and Travel Team

Related Blogs

Follow Us

Testimonials

Hear from students on why they chose the Trade and Travel Family and how it has changed their lives.