Before we start with the economic news update, Teri shared a few things last week at Blavity Fest 2025 in Atlanta that we think you’d appreciate.

She spoke about the importance of choosing the right brokers, making sure you’re using a platform that aligns with your trading goals and supports your needs. Teri also discussed the importance of choosing the right companies to invest in.

On top of that, she emphasized using stop losses to protect your money, so you’re not taking on more risk than necessary (especially important with how the recent tariff changes have caused a lot of market swings over the past couple of months).

Yet, what stood out most was her thoughts on margin accounts. Many people hear “margin” and think it’s just for big risk-takers, but Teri explained that margin accounts can actually give you more buying power and let you reinvest faster, as long as you understand how to manage the risk.

It’s not about going all-in recklessly, but about knowing when and how to use it to your advantage.

This is the kind of nuanced, practical advice that turns investing from something that feels overwhelming into something you can actually navigate. It’s a reminder that investing doesn’t have to be intimidating. It’s about learning the basics, one step at a time.

If you want to read more, here are two articles on Teri’s talk and the festival:

🔗 Blavity Fest at Atlanta’s West End (The Atlanta Voice)

🔗 The Blavity Fest Takeover (Streetz945ATL)

Let’s get into this week’s economic update!

Last week, major indices delivered a solid performance despite ongoing trade uncertainties. The S&P 500 (SPY) gained 1.65% for the week, while the tech-heavy Nasdaq (QQQ) outperformed with a 2.08% advance, and the Dow Jones (DIA) climbed 1.31%.

Market sentiment received a significant boost from the 90-minute phone call between President Trump and China’s President Xi, which helped ease concerns about an all-out trade war. The conversation established a framework for continued negotiations, with teams set to meet in London this week. Meanwhile, the European Central Bank delivered another 25 basis point rate cut, bringing rates to 2.00%.

U.S. employment data showed resilience with 139,000 jobs added in May, exceeding expectations of 126,000, while unemployment held steady at 4.2%. This solid labor market performance helped offset concerns about tariff impacts on economic activity.

Looking ahead to this week, market participants should brace for critical inflation data on Wednesday, with May CPI figures expected to provide the first clear signals of tariff-related price pressures.

📅 Wednesday, Jun 11th

- Core CPI m/m: The upcoming Core CPI month-over-month report will be closely watched as forecasts predict a 0.3% increase compared to the previous month’s reading of 0.2%, bringing the annual headline rate to approximately 2.4% year-over-year. This acceleration in core inflation, which excludes volatile food and energy prices, would represent a concerning uptick as it moves further away from the Federal Reserve’s comfort zone and could influence the central bank’s monetary policy decision at their June 17-18 meeting. Market participants and traders should particularly monitor whether the actual reading comes in above the 0.3% forecast, as this could signal persistent inflationary pressures that might delay anticipated Fed rate cuts.

- CPI m/m: The upcoming U.S. Consumer Price Index report for May is expected to show monthly headline inflation holding steady at 0.2% month-over-month, matching April’s reading. Market participants and traders should closely monitor whether the data reflects the first meaningful impact from increased tariffs on goods prices, particularly as this represents one of the final key economic releases before the Federal Reserve’s June 17-18 policy meeting where rates are widely expected to remain unchanged. Key areas of focus include shelter costs, which have been a primary driver of persistent inflation, and any signs of tariff-related price pressures in goods categories, as sustained inflation above the Fed’s 2% target could influence the central bank’s timeline for potential rate cuts later in 2025.

- CPI y/y: The upcoming Core CPI year-over-year report is expected to show an acceleration from 2.3% to 2.5%, marking a notable uptick in underlying inflation pressures as tariff-related costs begin filtering through to consumer prices. Market participants should closely monitor the monthly Core CPI reading, as this would represent the strongest monthly increase in four months and could signal persistent inflationary momentum. Again, key areas to watch include shelter costs, which have been the primary driver of core inflation, motor vehicle insurance prices, and core services excluding housing, as these components will determine whether the Federal Reserve maintains its cautious stance on interest rate policy.

📅 Thursday, Jun 12th

- Core PPI m/m: The upcoming Core PPI m/m report is forecasted at 0.3% compared to the previous reading of -0.4%, representing a significant potential swing from deflationary to inflationary pressures at the producer level. This 0.7 percentage point expected increase would mark a notable reversal from April’s largest monthly decline in the series’ history, when Core PPI fell sharply due to decreased service costs and trade margins. Market participants should watch for any deviation from the 0.3% forecast, as readings above expectations could strengthen the US dollar and signal mounting inflationary pressures that may influence Federal Reserve policy decisions, while weaker-than-expected data could weaken the dollar.

- PPI m/m: The upcoming Producer Price Index (PPI) month-over-month report, scheduled for release, is forecast to rise 0.2%, marking a potential reversal from April’s unexpected -0.5% decline. Market participants should scrutinize whether the rebound materializes in final demand services, particularly trade services margins (which fell 1.6% in April), and assess if producers begin passing tariff-driven input costs through to consumers, which could signal inflationary pressures ahead. A reading at or above 0.2% may reinforce expectations of Federal Reserve caution on rate cuts, while a miss could amplify concerns about weakening pricing power amid cooling demand in sectors like transportation and hospitality.

- Unemployment Claims: The upcoming initial jobless claims report for last week is forecasted at 241,000, representing a potential decrease from the previous week’s eight-month high of 247,000, which exceeded expectations of 236,000. Market participants should closely monitor whether the actual reading falls and if the four-week moving average, currently at 235,000, continues its upward trend, which signals labor market softening amid economic uncertainty from tariff policies. A reading significantly above 245,000 could trigger negative market sentiment and raise recession concerns, while a drop below 240,000 might provide relief that the recent uptick was primarily driven by Memorial Day holiday effects and seasonal school-year endings rather than fundamental economic deterioration.

📅 Thursday, Jun 13th

- Prelim UoM Consumer Sentiment: The University of Michigan’s Preliminary Consumer Sentiment report is expected to show a modest improvement to 52.5 from May’s final reading of 52.2, though this would still represent the fifth-lowest level since records began in 1952. Market participants should closely monitor whether tariff-related concerns continue to dominate consumer psychology, as nearly three-quarters of respondents spontaneously mentioned tariffs in May’s survey, up from 60% in April. Key areas to watch include any shifts in the current conditions versus expectations components, potential changes in inflation forecasts, and whether the temporary tariff pause on China goods continues to provide psychological relief to consumers.

- Prelim UoM Inflation Expectations: The University of Michigan’s preliminary inflation expectations report is forecast to remain at 6.6% for year-ahead expectations, inching up from 6.5% last month. Inflation expectations have surged dramatically from 2.6% in November 2024 to current levels, driven primarily by tariff concerns that were spontaneously mentioned by nearly three-quarters of consumers in recent surveys, representing a significant threat to the Federal Reserve’s price stability mandate. Market participants should closely monitor whether the reading exceeds the 6.6% consensus, as any upward surprise could signal persistent inflationary pressures that would reduce the likelihood of Federal Reserve rate cuts, while a decline below current levels might indicate that recent tariff pauses are helping to stabilize consumer price expectations.

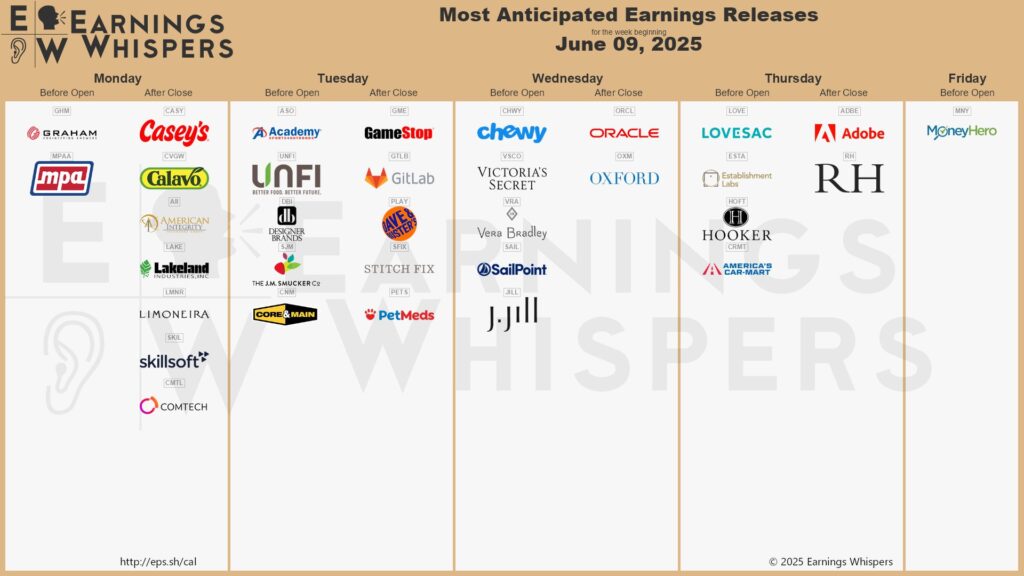

Here are some of the companies set to report earnings this week:

📅 Monday, Jun 9th

- Casey’s General Stores, Inc. (CASY): Casey’s is set to report its earnings, with analysts expecting earnings per share of $1.95 (down 16.6% year-over-year) and revenue of $3.93 billion (up 9.1% from the prior year). Market participants should closely monitor the integration progress of the $1.145 billion Fikes acquisition, which is expected to drive revenue growth but pressure margins due to integration costs, higher interest expenses, and an increase in operating expenses. Key metrics to watch include inside same-store sales growth, prepared food and dispensed beverage performance (projected to increase 13.2%), and management’s commentary on synergy realization from the 198 newly acquired Fikes stores.

📅 Wednesday, Jun 11th

- Oracle Corporation (ORCL): Oracle is scheduled to report its earnings, with Wall Street expecting earnings per share of $1.64 (up 0.6% year-over-year) and revenue of $15.57 billion (up 8.9% year-over-year). Market participants should focus on cloud momentum metrics, particularly Cloud Services and License Support revenue expected at $11.60 billion (13.4% growth) and Infrastructure cloud services projected at $6.70 billion (19.8% growth), as Oracle attempts to convert its record $130 billion Remaining Performance Obligations backlog into actual revenue. Key areas to monitor include AI infrastructure partnerships with major tech companies like OpenAI, Meta, and NVIDIA, data center capacity expansion progress, and whether Oracle can sustain the 49% cloud infrastructure growth rate achieved in its last quarter while addressing previous capacity constraints that limited revenue conversion.

- Chewy, Inc. (CHWY): Chewy will report its earnings on Wednesday, with analysts expecting earnings per share of $0.17 and revenue of approximately $3.07-3.08 billion, compared to the company’s guidance of $0.30-0.35 EPS and $3.06-3.09 billion in revenue representing 6-7% year-over-year growth. Market participants should closely monitor the company’s Autoship subscription penetration (which drove 80.6% of Q4 2024 net sales with 21.2% year-over-year growth), active customer growth (guided for mid-single-digit expansion), and margin expansion progress as Adjusted EBITDA margins reached 3.8% in the previous quarter. Key performance indicators to watch include net sales per active customer (NSPAC) growth, Chewy+ membership penetration, and the company’s ability to maintain strong customer retention rates while managing marketing spend within the 6-7% of sales target range.

📅 Thursday, Jun 12th

- Adobe, Inc. (ADBE): Adobe is set to report its earnings, with analyst consensus expecting earnings per share of approximately $4.97 and revenue of around $5.80 billion, representing year-over-year growth of roughly 10.7% and 9.2%, respectively. Market participants should closely monitor Adobe’s AI monetization progress, particularly the growth in its AI-first products. As of the end of Q1 FY 2025, these offerings had generated $125 million in ARR, and management expects this to double by the end of fiscal year 2025. Additionally, Adobe’s AI enhancements are already influencing over $3.5 billion in existing ARR, spanning its Creative and Document Cloud businesses. Monitoring whether Adobe meets its ambitious goal to double AI-related ARR within the next three quarters will be key to understanding its ability to monetize AI at scale. Key areas of focus will include Digital Media segment performance, Creative Cloud subscriber growth, forward guidance for the remainder of fiscal 2025, and commentary on competitive pressures in the rapidly evolving AI-powered creative tools landscape.

We hope this helps and happy trading!

– Trade and Travel Team

Related Blogs

Follow Us

Testimonials

Hear from students on why they chose the Trade and Travel Family and how it has changed their lives.