The stock market experienced a turbulent week as geopolitical tensions in the Middle East dominated headlines and influenced investor sentiment. Major indices closed the week in negative territory, with the S&P 500 (SPY) declining 0.46%, while the Nasdaq (QQQ) showed a marginal loss of 0.02%. The Dow Jones Industrial Average (DIA) dropped 0.25%.

The week began on a positive note, with Monday’s trading session seeing the Dow rise by 317 points (0.8%) as market participants initially shrugged off concerns about the escalating Israel-Iran conflict. However, sentiment quickly shifted as the situation in the Middle East deteriorated, with both nations targeting each other’s energy infrastructure and nuclear facilities. It’s good to observe how the market responds to geopolitical events that occurred over the weekend on Monday before deciding to take any trades.

On the economic front, the Federal Reserve maintained its benchmark interest rate at 4.25-4.5% during Wednesday’s FOMC meeting, citing continued economic expansion despite elevated inflation. This decision aligned with market expectations as the Fed remains cautious about the economic outlook.

Market participants should keep a close watch on several key events in the coming week. Fed Chair Jerome Powell’s two-day congressional testimony beginning Tuesday will be scrutinized for hints about future monetary policy. Friday brings the release of the Personal Consumption Expenditures (PCE) Price Index, a critical inflation indicator that could influence Fed decisions.

📅 Monday, Jun 23rd

- Flash Manufacturing PMI: The upcoming Flash Manufacturing PMI is expected to show a slight contraction to 51.1 from the previous reading of 52, indicating continued expansion in the manufacturing sector, albeit at a slower pace, as readings above 50 signal growth while those below suggest contraction. Investors should closely monitor key components, including new orders, production levels, employment, supplier deliveries, and input prices, as these sub-indices provide deeper insights into manufacturing health and potential inflationary pressures that could impact monetary policy decisions.

- Flash Services PMI: The upcoming U.S. Flash Services PMI is expected to register 52.9, a decline from the May final reading of 53.7. This signals a moderation in services sector growth while still remaining above the 50.0 threshold that indicates expansion. The 0.8-point decrease reflects a broader trend of cooling activity compared to the more robust growth seen in 2024. Although May showed a rebound from April’s dip, overall momentum has slowed this year. Market participants should keep an eye on three key factors. First, whether the actual reading meets expectations. Second, any commentary on input cost inflation, especially since recent tariff impacts have pushed price pressures to near two-year highs. Third, the employment component could provide insight into whether the current modest hiring pace, estimated at 0.1% monthly growth, can continue in the face of economic uncertainty.

📅 Tuesday – Wednesday, June 24th -25th

- Fed Chair Powell Testifies: Federal Reserve Chair Jerome Powell will testify before the House Financial Services Committee on Tuesday, June 24, as part of his semiannual Monetary Policy Report to Congress. He will then appear before the U.S. Senate Banking, Housing, and Urban Affairs Committee on Wednesday, June 25. Markets will be closely watching for signals on the Fed’s policy stance amid ongoing economic uncertainty.

Market participants should focus on Powell’s commentary regarding the current unemployment rate of 4.2%, inflation trends remaining above the Fed’s 2% target, and his assessment of tariff impacts on the economy. The Fed has held interest rates steady in the 4.25% to 4.5% range for four consecutive meetings and projects unemployment could rise to 4.5% by year-end.

Key metrics to monitor include Powell’s discussion of the 1.4% GDP growth projection for 2025, the potential timing of rate cuts (with markets expecting limited easing this year), and his guidance on how trade policy uncertainties and tariff-induced price pressures might influence the Fed’s dual mandate of maximum employment and price stability.

📅 Thursday, Jun 26th

- Final GDP q/q: The upcoming Final GDP q/q release is expected to confirm a second consecutive quarter of economic contraction at -0.2%, following the preliminary estimate that also showed a -0.2% decline, primarily driven by increased imports ahead of tariff implementations and weakening consumer spending. Market participants should closely monitor whether the data confirms a technical recession pattern, with particular attention to consumer spending figures which slowed to 1.2% in Q1 (the weakest pace since Q2 2023) and the potential impact on Federal Reserve policy, as policymakers have indicated they still anticipate two rate cuts in 2025 despite inflation concerns.

Market participants should also evaluate sectoral performance within the report for signs of resilience or further weakness, especially in manufacturing and services, while considering that the Conference Board has revised its 2025 GDP growth forecast from 2.8% in 2024 down to 1.6% from amid expectations of a “significant slowdown” rather than a full recession.

- Unemployment Claims: The Labor Department’s weekly initial unemployment claims report is forecast to show 247,000 new filings compared with 245,000 in the prior week, representing a 0.8% rise in claims expectations. Investors will watch whether actual claims exceed 247,000, which could signal cooling labor market resilience and pressure equity valuations, or come in below, reinforcing confidence in economic strength and supporting risk assets. Traders should also monitor the four-week moving average, currently at 245,500, to assess if the uptick is a one-time spike or the beginning of a broader trend in labor market softening.

📅 Friday, Jun 27th

- Core PCE Price Index m/m: The U.S. Core Personal Consumption Expenditures (PCE) price index is forecast to increase by 0.1% in June, matching May’s 0.1% rise and reflecting stable underlying inflation pressures. Investors should monitor whether the reading holds at 0.1% or surprises to the upside, as stronger-than-expected data could reinforce expectations for further Fed rate hikes. Traders will also pay close attention to the breakdown between goods and services components, as well as any upward revision to the prior month’s figure. Persistent service inflation could keep the Federal Reserve on a tighter policy path, which means restricting money flow by raising interest rates.

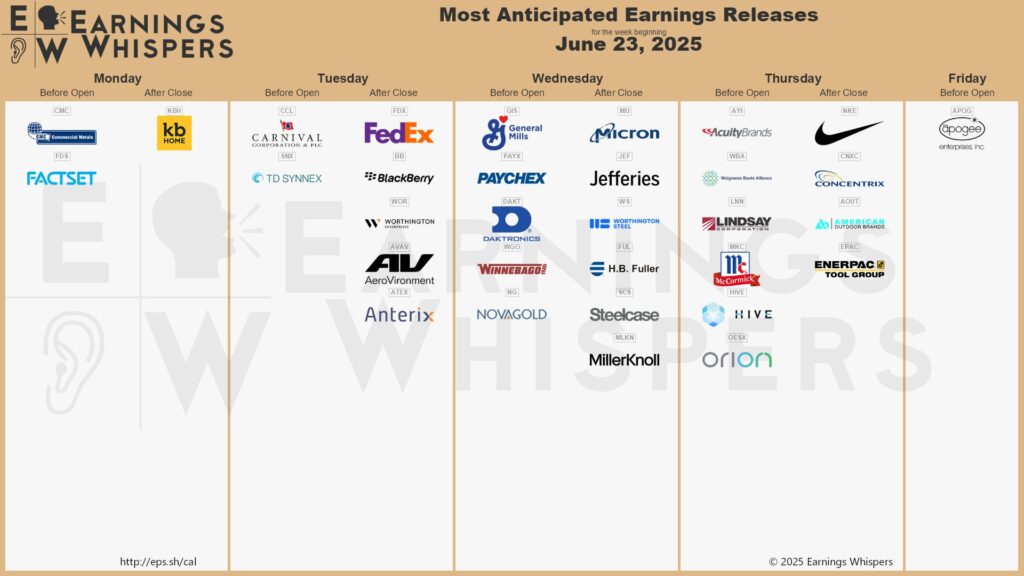

💼 Here are some of the companies set to report earnings this week:

📅 Tuesday, Jun 24th

- FedEx Corporation (FDX): FedEx is scheduled to report its fourth quarter fiscal 2025 earnings on Tuesday, June 24, 2025, after market close, with analysts projecting earnings per share of $5.88 (representing a 8.6% year-over-year increase) and revenue of approximately $21.79 billion, marking a slight 1.4% decline from the prior year period. Key metrics investors should monitor include the impact of the company’s DRIVE cost-reduction program, which has already delivered $600 million in savings during Q3 and remains on track to achieve its full-year target of $2.2 billion in permanent cost reductions for fiscal 2025, alongside volume trends in the Express segment where revenues are expected to remain soft with continued weakness in high-margin business-to-business shipments.

Critical guidance updates to watch include management’s revised full-year outlook calling for flat to slightly declining revenue and adjusted EPS of $18.00-$18.60 (down from previous expectations of $19.00-$20.00), while traders should also focus on progress toward the planned separation of FedEx Freight into a standalone public company within the next 18 months, which analysts believe could unlock significant shareholder value.

- Carnival Corporation (CCL): Carnival Corporation is set to release its earnings with analysts projecting earnings per share (EPS) of $0.25, a 127% increase from $0.11 in the year-ago quarter, and revenues of approximately $6.21 billion, up 7.4% year-over-year. Market participants should pay close attention to the company’s capacity utilization metrics, particularly Available Lower Berth Days (ALBDs), which is Number of lower berths × Number of cruise days, expected near 24 million, and net yields per ALBD, projected around $188, to gauge demand strength and pricing power within the leisure cruise segment. Additionally, scrutiny of onboard revenue growth, forecast to rise about 9% to $2.2 billion, will reveal the effectiveness of upselling strategies and cost-management initiatives heading into the summer peak season.

📅 Wednesday, Jun 25th

- Micron Technology, Inc. (MU): Micron Technology is set to report its earnings with analysts forecasting earnings per share of $1.59, more than double last year’s $0.62, and revenue of approximately $8.85 billion, up from $8.05 billion in Q2 2025, driven by AI‐related demand. Market participants should monitor guidance for fourth‐quarter revenue, currently expected near $9.92 billion, as well as margin commentary, given consensus pre‐tax profit projections of about $2.07 billion, to assess operational leverage amid memory cycle normalization, a return to stable demand and pricing in the memory chip market. Traction in high‐value segments such as HBM and data‐center DRAM, where DRAM revenue is projected to exceed $7.00 billion year-over-year, will be key for gauging the sustainability of this momentum and potential upside to consensus estimates.

- General Mills, Inc. (GIS): General Mills will release its earnings, with analysts forecasting adjusted EPS of $0.71, down 29.7% year over year, on revenues of $4.59 billion, a 2.5% decline from the prior-year period. Market participants should closely watch management’s commentary on organic net sales trends, particularly in North America Retail (projected by analysts at $2.71 billion, down 5%) and the Pet segment (projected at $646 million, up 7.3%), as well as any updates to full-year EPS guidance. Attention to revisions in analysts’ estimates in the days leading up to the call, and to the company’s discussion of promotional investments and margin pressures, will be key indicators of near-term stock reaction.

📅 Thursday, Jun 26th

- Nike, Inc (NKE): Nike is set to report its earnings with analysts expect revenue of roughly $10.71 billion, a 15% year-over-year decline from $12.61 billion and earnings per share of about $0.12, down 88% from $1.01 a year ago. Market participants should watch Nike’s reported revenue growth or decline versus the mid-teens sales drop guided by CFO Matt Friend (i.e., a decline of 13–17%,), gross margin contraction of 4–5 percentage points driven by inventory actions, and any adjustments to full-year guidance amid lingering tariffs, FX headwinds, and shifting consumer demand in key markets like China.

We hope this helps and happy trading!

– Trade and Travel Team

Related Blogs

Follow Us

Testimonials

Hear from students on why they chose the Trade and Travel Family and how it has changed their lives.