Market participants closed the shortened week on a broadly positive note as major U.S. indexes posted modest gains and reached fresh record highs. Optimism around trade negotiations, easing geopolitical tensions, and a dovish Federal Reserve outlook helped support sentiment.

As measured by tradable ETFs, the S&P 500 rose 1.70%, the Nasdaq-100 advanced 1.48%, and the Dow Jones Industrial Average gained 2.30% for the week, based on the performance of SPY, QQQ, and DIA, respectively.

On the policy front, Federal Reserve officials emphasized a data-driven approach to potential rate cuts. Comments from Fed Chair Jerome Powell and Governors Michelle Bowman and Christopher Waller signaled openness to easing later this year if inflation continues to moderate. This stance added further support to risk assets.

Looking ahead to the week of July 7, investors will focus on the Fed’s June meeting minutes expected on July 9. Trade deadlines on July 8 and 9, when reciprocal tariffs could be reimposed if no deal is reached, also remain in focus. In this environment, market participants will stay alert for volatility tied to tariff developments.

📅 Wednesday, Jul 9th

- FOMC Meeting Minutes: The Federal Open Market Committee (FOMC) will release the minutes from its June 17 to 18, 2025 meeting. These minutes will offer detailed insights into the Federal Reserve’s discussions during a key meeting where officials kept the federal funds rate in the current range of 4.25% to 4.50%. This marked the fourth consecutive meeting without a rate change since December 2024.

Market participants should pay close attention to three main areas. First is the Fed’s assessment of tariff impacts on inflation expectations, as officials project core PCE inflation to rise to 3.1% by year-end due to anticipated tariff effects. Second is the committee’s divided outlook on rate cuts, with seven of 19 participants now expecting no cuts in 2025 compared to four in March, even as the median still points to two 25-basis-point cuts later this year. Third is any indication about the timing of policy adjustments, especially in light of Chair Powell’s recent comment that the Fed would likely have cut rates by now if not for tariff uncertainty.

📅 Thursday, Jul 10th

- Unemployment Claims: The Department of Labor will release initial jobless claims for the week ending July 5, following the prior reading of 233,000 initial filings, which declined by 4,000 from 237,000 and came in below the 240,000 consensus forecast.

Market participants should monitor the four-week moving average of 241,500 claims, down 3,750 week-over-week, which smooths out volatility, as well as continuing claims holding at 1.964 million, the highest level since November 2021, signaling underlying labor market softness. A print above the 240,000 forecast could spark equity volatility, while persistently elevated claims may bolster expectations for a cautious Federal Reserve and drive allocations toward defensive sectors such as utilities and healthcare.

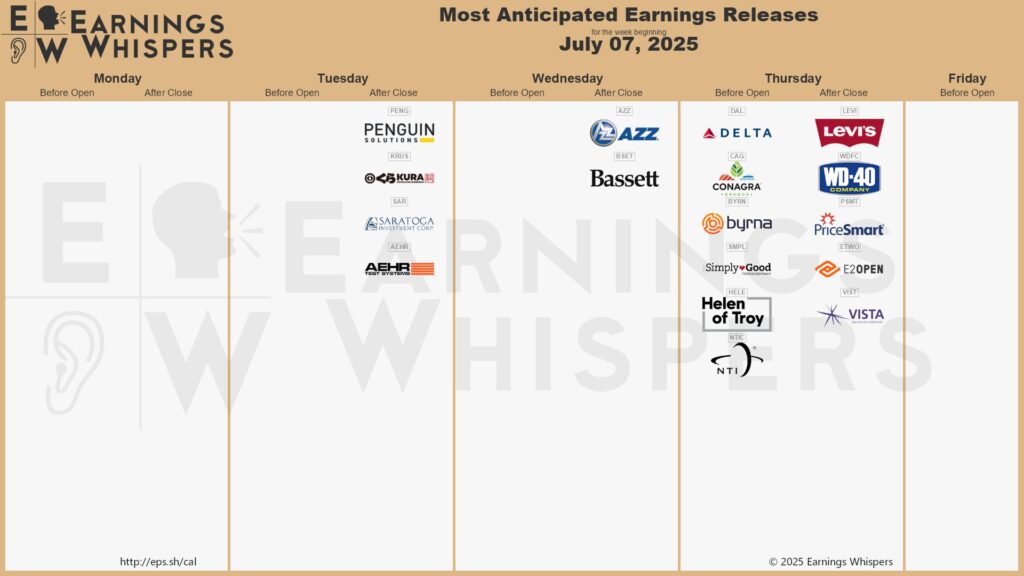

💼 As we wait for earnings season to ramp up, here are some early movers reporting this week:

📅 Thursday, Jul 10th

- The Simply Good Foods Company (SMPL): Simply Good Foods is set to release its Q3 fiscal 2025 results, and analysts currently forecast earnings of $0.50 per share on revenue of $381.7 million. Following a Q2 beat with EPS of $0.46 on $359.7 million in net sales, market participants will be watching management’s commentary on the balance between organic growth (previously +4.4%) and contributions from the OWYN acquisition, as well as any updates to full-year outlook calling for net sales growth of 8.5%–10.5% and adjusted EBITDA expansion of 4%–6%. Margin trends, particularly gross margin impacts from commodity costs and tariffs, and any shifts in net debt leverage (currently ~0.7× adjusted EBITDA) will also be key focal points for gauging financial discipline and future cash-flow trajectory.

- Levi Strauss & Co (LEVI): Levi Strauss & Co. is set to report Q2 results, with analysts forecasting earnings of $0.13 per share (–18.7% year-over-year) on revenues of $1.37 billion (–5.2% YoY). Market participants should focus on how actual EPS compares to the $0.13 consensus and whether top-line performance in direct-to-consumer versus wholesale channels drives margin expansion or contraction. Attention should also center on any commentary regarding full-year 2025 adjusted EPS guidance of $1.20–$1.25, and potential revisions to near-term revenue and margin outlooks.

- Delta Air Lines, Inc. (DAL): Delta Air Lines will report Q2 2025 results, with analysts forecasting EPS of $2.06 (–12.7% YoY) on revenue of $15.44 billion (+0.2% YoY). Market participants should focus on management’s guidance, EPS range $1.70–$2.30 and operating margin target of 11–14%, and any commentary on cost per available seat mile (CASM) trends, particularly fuel-adjusted CASM efficiency. Sentiment on premium travel mix and loyalty-program revenue (up ~13% YoY in Q1) will also be critical indicators of margin resilience amid softer main-cabin demand.

- ConAgra Brands, Inc. (CAG): Conagra Brands is set to release Q4 2025 results, with analysts forecasting earnings of approximately $0.58 per share (down ~4.9% year-over-year from $0.61) on revenue of about $2.83 billion (a 2.7% decline). Market participants should focus on whether management can offset elevated input‐cost inflation, with sequential improvements in productivity and volume restocking in frozen and snacks channels. Attention will also center on organic net sales growth trends and any commentary on foreign‐exchange headwinds, as these factors will indicate the durability of Conagra’s cost‐management initiatives heading into fiscal 2026.

We hope this helps and happy trading!

– Trade and Travel Team

Related Blogs

Follow Us

Testimonials

Hear from students on why they chose the Trade and Travel Family and how it has changed their lives.