The final trading week of 2025 tested investor patience as the S&P 500, Nasdaq, and Dow Jones all retreated from record highs established the previous week.

The SPY (S&P 500) declined 1.03%, the QQQ (Nasdaq-100) fell 1.73%, and the DIA (Dow Jones Industrial Average) dropped 0.70% for the week, reversing the positive momentum of the earlier holiday-shortened week, when stocks had kicked off what initially looked like a Santa Claus rally, although by the end of that period analysts noted that a traditional Santa Claus rally had not fully materialized.

Despite the loss, all three major indices finished the year up substantially. The S&P 500 is up 16.39%, the Nasdaq is up 20.36%, and the Dow is up 12.97%, marking the third consecutive year of double-digit gains for the broad market.

The week’s decline followed the release of the Federal Reserve’s December meeting minutes on Dec. 30, which showed a closely contested policy discussion. The minutes revealed significant disagreements among officials over the pace and extent of future rate cuts, reflecting differing views on how best to balance a slowing labor market with ongoing inflation risks.

The FOMC approved a quarter-percentage-point rate cut by a 9-3 vote on December 10, the highest number of dissenting votes since 2019, with officials expressing caution about the pace of future reductions. Minutes disclosed that while most participants believed further cuts would likely be warranted if inflation declined as anticipated, the committee has adopted a decidedly wait-and-see posture, effectively signaling that any additional rate reduction would require fresh economic data justifying such action.

The hawkish tone around rate-cut timing disappointed equity traders who had been pricing in multiple 2026 cuts, with some expectations exceeding what the Fed’s December projections suggested. Markets subsequently repriced expectations downward, with traders now broadly accepting that the Fed will maintain rates in the 3.50-3.75 percent range through at least the first quarter of 2026.

The government’s economic recovery narrative remained supportive despite market weakness. The third-quarter GDP report, released early in the week due to the government shutdown’s impact on data scheduling, showed the economy expanding at a robust 4.3% annualized rate, crushing consensus expectations by over a full percentage point and marking the strongest quarterly growth in two years.

Industrial production accelerated to 2.5% year-over-year in November, the strongest pace since September 2022, signaling underlying economic vitality despite periodic bouts of market volatility. Weekly jobless claims moved lower, though hiring remains sluggish relative to pre-pandemic patterns, creating the textbook backdrop for the Fed’s balanced-approach stance.

As January unfolds, market participants will be watching several key developments. The Q4 earnings season begins in mid-January, giving management teams a platform to discuss full-year 2026 guidance amid lingering macro uncertainty. Any clarification on tariff policy or major fiscal initiatives, including speculative proposals like $2,000 tariff dividend checks, could spur market repricing, and geopolitical developments will likewise be key catalysts.

How This Impacts You

With the market still moving in an uncertain but active environment, this is a good moment to practice staying steady while you learn how the market behaves. Choose one time of day this week, morning or evening, and spend just five minutes looking at the overall market index instead of a single stock.

Notice whether the market feels calm, quiet, or jumpy, and write down one sentence about how that tone makes you feel. This helps you build emotional awareness and confidence before you ever place your first trade.

📅 Monday, Jan 5th

- ISM Manufacturing PMI: The U.S. ISM Manufacturing PMI is set to be released, with consensus forecasts calling for a modest 0.1-percentage-point uptick to 48.3 from December’s reading of 48.2, keeping the sector squarely in contraction territory below the 50-point expansion threshold.

Investors and traders should closely monitor the employment index (previous 44.0) and new orders subcomponent (previous 47.4), as both have deteriorated significantly and signal sustained weakness in hiring and demand despite December’s better-than-expected headline PMI surprise of 51.8 from S&P Global.

The prices paid index, forecast at 59.0 versus December’s 58.5, will be critical to watch for inflationary signals that could influence Federal Reserve policy considerations, particularly as manufacturing has now contracted for nine consecutive months. A reading below the 48.3 forecast could reinforce recessionary concerns, while an unexpected surge above 50.0 could spark risk-on sentiment.

📅 Wednesday, Jan 7th

- ADP Non-Farm Employment Change: The ADP Non-Farm Employment Change report will provide a critical gauge of private-sector hiring momentum, with economists forecasting a gain of 47K positions after November’s unexpected decline of 32K jobs marked the steepest drop in over two years.

The weakness was driven mainly by small establishments, which shed roughly 120,000 jobs, while large firms added around 39,000 positions, highlighting uneven labor market dynamics. Investors and traders will be watching whether this continued softness in private hiring persists in the coming reports.

A forecast beat would ease recession concerns and likely strengthen Fed rate-cut expectations, while a miss below 40K could accelerate equity volatility and signal the labor market is cooling faster than policymakers anticipated. Watch the composition by firm size closely: large company hiring resilience versus continued small business contraction will determine whether weakness is concentrated or broadening across the private sector.

- ISM Services PMI: The next ISM Services PMI is scheduled for release, with the headline expected to slip to 52.3 versus a prior 52.6. With 50.0 as the expansion line, 52.3 would still imply services growth, but the 0.3-point step down would reinforce a modest cooling in momentum.

Market participants should focus on whether demand is broadening, especially if New Orders and Business Activity stay above 50.0, or if either falls toward 50.0, which would raise recession-scare sensitivity in rates and cyclicals. Inflation implications matter as much as the headline, so watch Prices Paid, where a print above 60.0 would look “sticky”, while a move toward 55.0 would be read as disinflation progress.

- JOLTS Job Openings: The upcoming JOLTS report is expected to show job openings moderating slightly to 7.65 million from the previous reading of 7.67 million, signaling a continued stabilization rather than a sharp contraction in labor demand.

Market participants should scrutinize whether the ratio of vacancies to unemployed workers holds steady, as a significant dip could reignite recession fears and aggressively price in Federal Reserve rate cuts. A print above expectations would conversely reinforce the soft-landing narrative, suggesting businesses remain confident enough to maintain open roles despite restrictive rates.

Traders need to specifically watch the quits rate for signs of waning worker confidence, which often precedes broader consumption slowdowns. Ultimately, a figure aligning with the 7.65 million forecast would likely support a neutral market reaction, while a deviation of more than 200,000 could trigger volatility in Treasury yields and risk assets.

📅 Thursday, Jan 8th

- Unemployment Claims: The next report will report initial jobless claims for last week, with a previous reading of 199K and consensus forecast of 216K, representing a potential 8.5% increase that warrants close attention from equity and fixed-income markets.

A miss above 216K would signal labor market deterioration and intensify recession concerns, likely triggering a flight to safer assets, including Treasury bonds and defensive equities, while pressuring equities and the dollar. Conversely, a print closer to or below the previous 199K would reinforce the “no-hire, no-fire” labor market trend documented through 2025, supporting Fed pause expectations and benefiting risk assets.

Traders should monitor the 4-week moving average, which has remained relatively stable near 218K, as sustained upward momentum above 225K could alter Federal Reserve rate-cut expectations. The continuing claims figure, which recently declined to 1,866K from 1,913K, provides a secondary confirmation signal for labor market health and should also be scrutinized, as sustained weakness in this metric could prompt more aggressive market repricing of growth and inflation outlooks.

📅 Friday, Jan 9th

- Average Hourly Earnings m/m: The December Average Hourly Earnings m/m report will be closely watched for signs of shifting wage pressure. November’s modest 0.1% gain underscored easing wage growth, and even a slightly stronger December print could influence inflation expectations and Fed policy pricing.

A beat above 0.3% would suggest the job market is still tight and wages are rising faster than expected. That could worry the Federal Reserve, because stronger wage growth can keep inflation higher, and it may lead them to keep interest rates higher for longer than the market expects.

On the other hand, if the number comes in below 0.3%, especially at 0.2% or lower, it would support the view that wage growth is slowing. That would give the Fed more confidence that inflation is easing toward its 2% target. Year-over-year wage growth stands at 3.5%, marking the slowest pace since May 2021, which offers some relief for inflation-conscious traders.

- Non-Farm Employment Change: The December Non-Farm Payroll report scheduled for release follows a weak November print of 64,000 jobs. Economists expect continued modest job gains, reflecting ongoing softness in labor demand.

After a year of subdued hiring and elevated uncertainty in the U.S. economy, the December jobs figure will be closely watched for further signs of labor market momentum. The forecast of 57,000 represents a modest 7,000 job decline from the previous month and reflects declining hiring momentum that has characterized the second half of 2025.

Investors should monitor whether the actual print falls significantly below the 57,000 forecast, as any substantial miss could reinforce recession concerns, while a beat would suggest labor market resilience and potentially delay the Federal Reserve’s interest rate cutting cycle.

- Unemployment Rate: The unemployment rate is expected to hold or tick down modestly to 4.5% from November’s 4.6%, but any reading that edges toward 4.7% or higher would signal an acceleration in labor slack that contradicts the Fed’s December projection of stabilization at 4.5%.

Investors should closely track jobless claims data and sector composition when released, particularly weakness in healthcare and retail relative to recent trends, as a loss of momentum in traditionally resilient hiring segments would amplify recessionary signals.

Given the elevated sensitivity of VIX and equity volatility to unemployment surprises rather than directional returns alone, expect short-term price swings if the report deviates materially from the 4.5% forecast, with bears using any weakness to support lower valuations in early 2026.

- Prelim UoM Consumer Sentiment: The University of Michigan Preliminary Consumer Sentiment Index is expected to rise to 53.5, suggesting slightly improved confidence after several months of subdued sentiment. While sentiment remains historically subdued, households continue to report concerns about prices and labor-market conditions. Year-ahead inflation expectations are still elevated relative to pre-pandemic norms, and uncertainty about unemployment prospects is weighing on overall confidence.

Traders should watch how the subcomponents behave in the preliminary January report, specifically whether the Current Economic Conditions index (50.4 in December) and the Index of Consumer Expectations (54.6 in December) both improve or whether gains are concentrated in one component.

Persistent weakness in durables-buying conditions and long-run inflation expectations near 3.2% suggest consumer caution remains entrenched. A preliminary print below the recent 52.9 level would likely reinforce concern about consumer confidence, while a stronger-than-expected result would need to be viewed in the context of other data, including labor market trends and broader price pressures, before signaling a durable rebound.

- Prelim UoM Inflation Expectations: The University of Michigan’s preliminary one-year inflation expectations fell to 4.2% in December 2025, marking the lowest reading in nearly a year after declining for four consecutive months from the November level of 4.5%.

The preliminary estimate came in above the 4.1% forecast but was revised slightly upward, signaling persistent consumer inflation concerns despite the downward momentum. Concurrently, five-year inflation expectations eased to 3.2%, reaching a near one-year low and aligning with the preliminary reading, down from 3.4% in November.

Market participants should monitor whether this fourth consecutive monthly decline represents a sustained deceleration in inflation expectations or merely reflects seasonal volatility heading into 2026. The gap between the 4.2% one-year and 3.2% five-year readings suggests consumers remain cautious about near-term pricing pressures while maintaining confidence in the Fed’s longer-term inflation control.

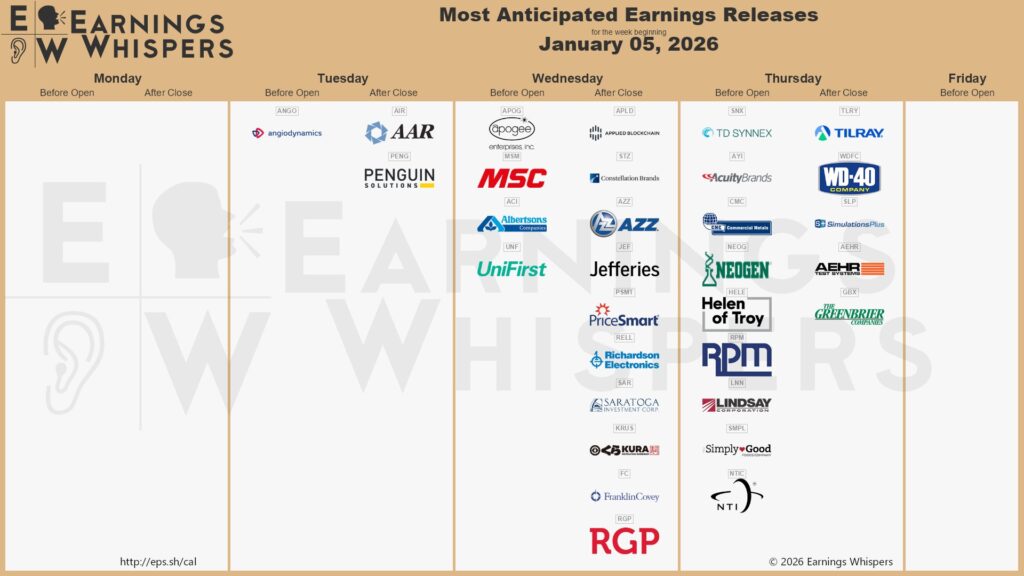

💼 As we head into the first full trading week of 2026, the earnings calendar remains relatively light, but a handful of early reports could still act as catalysts for short-term market moves.

📅 Wednesday, Jan 7th

- Albertsons Companies, Inc. (ACI): Albertsons Companies is scheduled to report its Fiscal 2025 Q3 earnings. Analysts have set a consensus earnings per share (EPS) estimate of roughly $0.68, reflecting a slight year-over-year decline from $0.71 in the comparable period, as the grocer navigates normalized consumer demand.

Revenue is projected to reach approximately $19.17 billion, marking a modest ~2% increase driven by food inflation and steady traffic. Investors will scrutinize Identical Sales growth, looking for a figure above 2% to confirm that volume is holding up despite competitive pricing pressures from rivals like Walmart. Digital Sales remain a critical growth engine; investors will be watching for continued double-digit growth after the company reported 25% year-over-year digital sales growth in Q1 2025.

With the Kroger merger termination now over a year in the past (Dec 2024), the market’s primary focus has shifted entirely to ACI’s standalone “Plan B” strategy and operational efficiency. Traders should watch for updates on the ongoing litigation regarding the $600 million merger breakup fee, which remains a potential cash windfall or legal overhang. Gross margin performance will be a key indicator of how well Albertsons is managing higher labor costs and “shrink” (inventory theft) without the scale benefits of a combined entity.

Pay close attention to capital allocation updates, specifically the pace of the $2 billion share repurchase program authorized post-merger, as support for the stock price. Finally, forward guidance for Fiscal 2026 will be paramount; investors need reassurance that the company can sustain profitability growth in a disinflationary environment without M&A catalysts.

- Constellation Brands, Inc. (STZ): Constellation Brands will report its Q3 fiscal 2026 results, with Wall Street consensus expecting adjusted EPS of $2.64 per share, down 18.7% year-over-year from $3.25 in the prior-year quarter, reflecting ongoing macroeconomic headwinds and volume softness. Revenue is projected at $2.16 billion, down 12.1% versus the prior-year quarter’s $2.46 billion, driven primarily by weakness in the wine and spirits segment following divestitures of SVEDKA and lower-end wine brands.

Constellation Brands’ beer segment is expected to show a modest year-over-year sales decline in Q3, consistent with recent guidance for weaker beer net sales in fiscal 2026. Analysts and company commentary cite margin pressures from tariffs and fixed costs, along with volume softness, particularly among key Hispanic consumer segments, as ongoing headwinds for profitability.

The wine and spirits business is anticipated to report net sales of approximately $170 million, a 60.5% collapse year-over-year, with operating income expected near break-even at around $10.9 million versus $95.2 million in Q3 2025. Consensus estimates point to continued softness in wine and spirits demand amid the company’s ongoing portfolio rationalization and divestiture activity.

Investors should focus on three key catalysts: (1) whether pricing strategies and marketing investments can stabilize volume declines in the core beer business, (2) inventory levels and distributor dynamics given management’s prior statements about achieving equilibrium in the second half, and (3) management’s commentary on consumer sentiment among Hispanic populations, who represent a critical demographic facing financial pressures.

- Jefferies Financial Group Inc. (JEF): Jefferies Financial Group will report its Q4 and annual 2025 financial results, with analysts projecting EPS of $0.83, a 21% year-over-year decline, on revenues of approximately $1.93 billion, down 1.1% from the prior-year quarter.

The anticipated EPS decline stands in sharp contrast to Jefferies’ exceptional Q3 performance, when the firm reported $1.01 in diluted EPS, beating consensus estimates of $0.80 by 26%, driven by record investment banking advisory revenues and robust capital markets activity. Investors should closely monitor Total Investment Banking and Capital Markets net revenues, which analysts expect to reach $1.86 billion, representing a 13.8% increase year-over-year, powered by anticipated growth in debt underwriting (+32.9%), equity underwriting (+50.6%), and advisory revenues (+6.9%).

Jefferies’ recently filed segment results underscore the contrast between its comparatively resilient investment banking and capital markets performance and the weaker asset management outcomes, reflecting uneven exposure to market conditions in 2025. Market commentary and analyst reports have tied volatility in deal activity earlier in the year to tariff-related uncertainty and broader macro risks.

The Q4 report will provide crucial guidance on the firm’s positioning relative to peers as global M&A volumes are estimated to reach $4.8 trillion in 2025, up 36% in value, creating favorable tailwinds for advisory revenue for the year as a whole, but raising questions about Q4’s specific contribution to this figure.

📅 Thursday, Jan 8th

- TD SYNNEX Corporation (SNX): TD SYNNEX is scheduled to report its Fiscal 2025 Q4 and full-year earnings. Wall Street consensus estimates project revenue of approximately $16.95 billion, aligning with management’s guidance range of $16.5 billion to $17.3 billion. Analysts anticipate non-GAAP earnings per share (EPS) to come in around $3.73, firmly within the company’s forecasted band of $3.45 to $3.95.

Investors should focus on the performance of the Hyve Solutions unit, which has become a critical growth engine due to surging demand for AI infrastructure and hyperscale data center deployments. Management previously projected non-GAAP gross billings to grow approximately 11% year-over-year to between $23.0 billion and $24.0 billion, a key indicator of underlying IT spending momentum.

Following a third quarter where revenue rose 6.6% to $15.65 billion, traders will be looking for continued acceleration in the Endpoint and Advanced Solutions segments. Operating margins will be a focal point, as investors seek confirmation that the company is successfully capitalizing on high-value technology shifts while managing operational costs.

- Acuity Inc. (AYI): Acuity Brands will report its Q1 fiscal 2026 earnings with consensus estimates calling for EPS of $4.60 on revenue of $1.144 billion. The EPS forecast implies an ~11.5% sequential decline from the prior quarter’s $5.20 beat, consistent with normal seasonal patterns in the business. Investors should monitor whether management reiterates its full-year 2026 EPS guidance of $19.00–$20.50 and revenue guidance of $4.7–$4.9 billion, which would imply 10% full-year earnings growth.

Acuity’s traditional Lighting segment is expected to deliver low-single-digit growth in fiscal 2026, a pace that likely outpaces the broader lighting market’s flat to modest growth trends, suggesting potential market share gains. Analysts and management commentary cite modest pricing actions and operational efficiencies as key levers supporting this performance.

The Intelligent Spaces division, powered by the $1.2 billion QSC acquisition completed in May, remains the growth catalyst. Q4 fiscal 2025 demonstrated this with Acuity’s Intelligent Spaces (AIS) segment sales surging 204% to $255 million, though adjusted operating margins compressed 420 basis points to 21.4% due to integration and margin profile differences.

Traders should focus on management commentary regarding margin trajectory recovery timelines, AIS integration progress, and any updates on tariff pass-through assumptions, as recent quarters have demonstrated that Acuity’s margin expansion narrative depends critically on the successful execution of its industrial tech pivot.

We hope this helps and happy trading!

– Trade and Travel Team

Related Blogs

Follow Us

Testimonials

Hear from students on why they chose the Trade and Travel Family and how it has changed their lives.