The stock market staged a powerful recovery last week, with all three major indices closing solidly higher following renewed optimism around Federal Reserve policy. The S&P 500 (SPY) gained 3.70% for the week, while the Nasdaq-100 (QQQ) led the charge with a 4.95% advance, and the Dow Jones Industrial Average (DIA) climbed 3.16%. This rebound proved particularly significant given the market’s struggle in recent weeks.

Monday’s session set a positive tone for the week, as U.S. stocks advanced on rising expectations that the Federal Reserve could cut interest rates at its December meeting. Markets were supported by comments made days earlier by New York Fed President John Williams, who indicated that monetary policy remained restrictive and that further adjustment could be warranted. As a result, investors grew more confident that policy easing could continue, fueling gains across major indexes and supporting risk-asset sentiment.

Technology stocks, including several AI-related names, rebounded alongside the broader market after recent weakness. Gains were more widely distributed, with financial services and industrials also advancing, reflecting improving risk appetite as investors responded to easing rate expectations and signs of continued earnings resilience.

As markets head into December, investors will closely monitor corporate earnings guidance, labor market developments, and inflation data to validate current optimism. The December Federal Reserve meeting on December 9-10 remains a pivotal event, with the market pricing in meaningful support for equities if the Fed follows through on rate reduction expectations. For traders and investors, the week demonstrated that sentiment can shift decisively on policy clarity, reversing weeks of accumulated losses and setting a potentially bullish tone for the year-end seasonal period.

How This Impacts You

The market’s recent rebound is a good reason to start building the habit of watching the market. Create a free CNBC account and add SPY (S&P 500), QQQ (Nasdaq-100), and DIA (Dow Jones Industrial Average) to your watchlist to track how the overall market moves. Choose one day each week to check in and make note of what you see. Keep a simple log of your observations so it becomes part of your routine.

📅 Monday, Dec 1st

- ISM Manufacturing PMI: The upcoming ISM Manufacturing PMI report will reveal December 2025 conditions for the US manufacturing sector following October’s reading of 48.7, with consensus forecasting an uptick to 49.0, remaining entrenched in contraction territory below the 50 expansion threshold.

While a 0.3-point improvement would signal stabilizing activity after persistent weakness throughout the year, market participants should scrutinize whether new orders are rebounding and inventory levels are normalizing, as these subcomponents often precede broader manufacturing recovery. The reading holds particular significance given manufacturing’s role as a leading economic indicator ahead of GDP data and employment figures, with potential to shift investor sentiment regarding corporate earnings and Federal Reserve policy trajectories.

📅 Wednesday, Dec 3rd

- ADP Non-Farm Employment Change: The upcoming ADP Non-Farm Employment Change report, with economists forecasting a significant deceleration to 19,000 jobs added compared to October’s 42,000 gain, representing a potential 55% slowdown in private-sector hiring momentum.

This expectations reflects broader market concerns about labor market weakening, particularly following recent weekly ADP data showing private employers shed an average of 13,500 jobs per week in the four weeks ending November 8. The wage growth component remains critical, with job-stayers’ annual pay growth holding flat at 4.5% and job-changers’ pay at 6.7%, suggesting balanced labor supply and demand dynamics that could influence Federal Reserve policy expectations if hiring continues deteriorating.

- ISM Services PMI: The ISM Services PMI serves as a critical barometer for U.S. economic health since services comprise nearly 80% of the economy, and investors should closely monitor whether the reading declines from the previous month’s robust 52.4 to the forecasted 52.0 or delivers a surprise in either direction.

A decline to 52.0 would signal a moderation in service sector expansion, particularly important given the ongoing employment contraction that registered 48.2% in October, suggesting businesses lack confidence in sustained economic strength despite resilient new orders and business activity.

Traders should focus on the sub-components, especially the Business Activity Index and New Orders Index, as these reveal whether the slowdown reflects seasonal adjustment or a genuine loss of momentum heading into 2026. Any reading below the 50-point breakeven threshold would signal service sector contraction, while a beat above 52.0 could provide support for equities and signal resilience against tariff and fiscal policy headwinds.

📅 Thursday, Dec 4th

- Unemployment Claims: The upcoming Initial Unemployment Claims report is projected to show a slight increase to 220,000 from the prior 216,000 which would signal a labor market that is normalizing but not collapsing. Market participants should view this data through the lens of the upcoming Federal Reserve policy meeting since a figure near the 220,000 forecast would reinforce the case for policymakers to pause interest rate cuts.

📅 Friday, Dec 5th

- Core PCE Price Index m/m: The upcoming Core Personal Consumption Expenditures Price Index m/m reading holds critical importance as it tracks whether inflation is finally stabilizing after months of progress toward lower inflation, followed by a recent period of stabilization above the Fed’s 2.0% target.

With the previous reading at 0.2% and forecasts pointing to another flat 0.2% m/m increase, a matching result would suggest underlying price pressures remain locked in place, neither accelerating nor showing meaningful progress toward Fed officials’ preferred trajectory.

Traders should closely monitor this data point because any deviation from the 0.2% forecast could significantly influence near-term monetary policy expectations. The stalled monthly pace matters more than the headline because it filters out volatile food and energy components, revealing whether the sticky service-side inflation that has persistently resisted Fed efforts is finally cooling.

Should the report come in flat at 0.2%, investors may interpret this as confirmation that inflation has plateaued around 2.8-2.9% annually, keeping policy rate cut expectations on hold or potentially shifting focus toward labor market weakness rather than inflation concerns.

- Prelim UoM Consumer Sentiment: The Preliminary University of Michigan Consumer Sentiment report is expected to increase from the November final reading of 51.0 to a forecast of 52.0, signaling modest consumer optimism recovery.

Market participants should pay close attention to the Index of Consumer Expectations, which tracks household financial outlooks and broader economic prospects and is widely regarded as a forward-looking indicator of economic trends. The Current Economic Conditions Index is also important to watch, after weakening sharply in recent months, any stabilization would signal easing pessimism around present financial conditions and consumers’ willingness to spend on big-ticket items.

- Prelim UoM Inflation Expectations: The University of Michigan’s preliminary inflation-expectations data, based on a monthly survey of U.S. households, showed that consumers’ year-ahead inflation outlook edged up to 4.7% in early November from 4.6% in October, according to the preliminary report. While this marked a small increase, expectations remain below the 4.9% level recorded in August and far from the mid-2025 highs, when inflation concerns peaked earlier in the year.

Longer-term expectations moved in the opposite direction. The survey’s five-year inflation outlook declined to 3.6% in the preliminary November reading, down from 3.9% in October, and was later revised lower to 3.4% in the final report, indicating that consumers continue to view longer-term inflation as relatively more stable than near-term price pressures. Because this series is often revised meaningfully between preliminary and final releases, Market participants continued to monitor both readings closely for changes in consumer sentiment around future pricing trends.

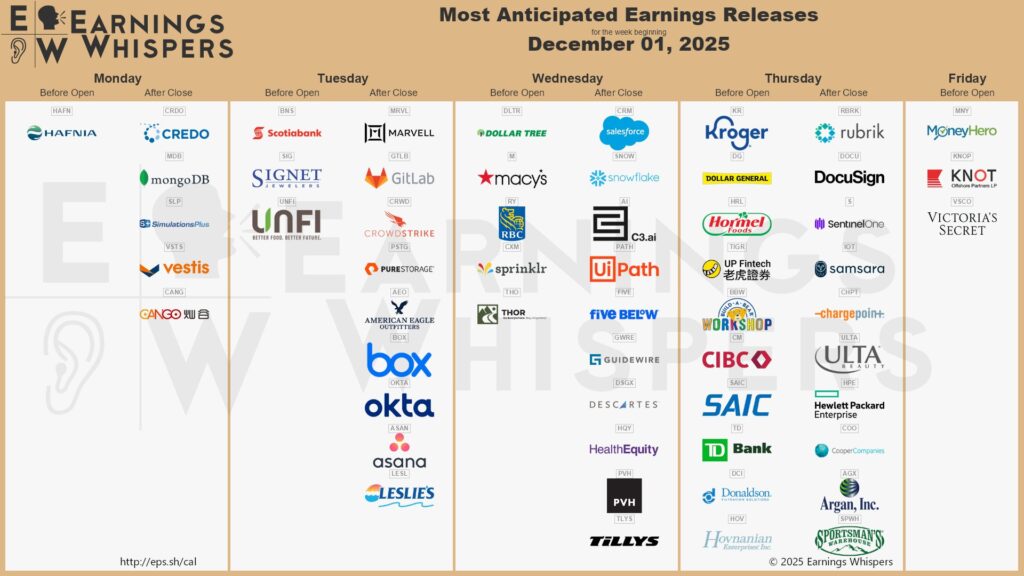

💼 A slow earnings week, but guidance from consumer and tech companies could still drive short-term moves.

📅 Monday, Dec 1st

- MongoDB, Inc. (MDB): MongoDB is scheduled to report fiscal Q3 2026, with investors closely watching how its momentum may hold up after earlier guidance-related volatility. Consensus estimates point to revenue of roughly $593 million, implying about 12% year-over-year growth and placing expectations near the top of management’s $587–592 million guidance range. EPS is projected around $0.80–$0.81, roughly 30% below last year’s $1.16, which appears to reflect softer margin expectations even as the company continues to invest in Atlas and AI-related capabilities.

A central focus is expected to be Atlas, which made up 74% of revenue last quarter and grew 29% year over year. Investors will likely be watching whether Atlas growth once again outpaces the roughly 12% overall revenue growth that analysts anticipate and may also pay close attention to non-Atlas subscription trends and multiyear deals, which management has previously described as softer than Atlas, to assess how much they may be weighing on overall subscription growth.

Looking ahead, management’s Q4 and full-year fiscal 2026 guidance on revenue and earnings, along with any commentary around pipeline strength or win rates, is likely to have a larger impact on the stock than whether Q3 results simply exceed or fall short of consensus. Customer metrics, particularly the number of customers generating more than $100,000 in annual recurring revenue, will also be closely watched as a potential indicator of large-enterprise adoption and competitive positioning. The most recent figure stood at 2,564 customers, up from about 2,506 in the prior quarter.

📅 Tuesday, Dec 2nd

- CrowdStrike Holdings, Inc. (CRWD): CrowdStrike is scheduled to report quarter ending October, with consensus calling for about $0.94 in EPS on revenue of roughly 1.21–1.22 billion, up around 20% year over year. Investors will benchmark those numbers against last quarter’s revenue of about 1.17 billion, which grew roughly 19.8% year over year, and EPS of $0.93, both of which came in ahead of expectations, to judge whether growth momentum is holding or decelerating.

Street estimates imply about $1.16 billion in subscription revenue and roughly $58.5 million in professional services revenue, which would translate into around 20% growth in subscriptions and low-20s percent growth in services, making any shift in the mix an important signal for demand strength. Platform adoption remains central, with attention on the percentage of customers buying five or more modules and on ARR from cloud security, identity protection, and next-generation SIEM (Security Information and Event Management), which recently surpassed $1.3 billion in aggregate and has been growing at close to a 50% blended annual rate.

📅 Wednesday, Dec 3rd

- Salesforce, Inc. (CRM): Salesforce will report Q3 fiscal 2026 results, with consensus expectations calling for EPS of $2.86 per share compared to $2.41 in the year-ago quarter, representing a 18.6% YoY increase. Revenue is projected to reach $10.27 billion, reflecting approximately 8.8% YoY growth, within the company’s guidance range of $10.24 billion to $10.29 billion, though this represents a notable deceleration from the 9.8% growth delivered in Q2.

The earnings report arrives at a key moment as investors evaluate whether Salesforce’s AI platform, Agentforce, can generate meaningful revenue over time and support the company’s premium valuation. Current Remaining Performance Obligation growth is also in focus and is expected to run slightly above 10% year over year, reinforcing confidence in durable demand and future revenue visibility, with early contributions from AI-related offerings such as Agentforce and Data Cloud beginning to appear in longer-term contract activity.

Agentforce adoption will be in focus, with Salesforce reporting that the platform has generated more than 12,500 total deals since launch, including over 6,000 paid agreements. In the most recent quarter, the company also said that over 40% of Data Cloud and Agentforce bookings came from expansion within existing customers, underscoring growing traction across its installed base.

Another key metric to monitor is Data Cloud and AI annual recurring revenue, which surpassed $1.2 billion in the second quarter, representing approximately 120% year-over-year growth. While still a small portion of the business overall, this fast-growing segment is becoming increasingly important within Salesforce’s $29.4 billion of current remaining performance obligations.

- Snowflake Inc. (SNOW): Snowflake is scheduled to report Q3 2026 earnings marking a critical juncture for evaluating the company’s trajectory amid AI-driven data cloud adoption. Wall Street consensus expects $0.31 EPS and $1.18 billion in revenue, representing approximately 25.6% year-over-year revenue growth and a 55% improvement in EPS compared to the year-ago quarter.

Analysts expect Snowflake to generate about $1.13 billion in product revenue, implying mid-20% year-over-year growth, with product gross profit implied in the mid-$800 million range based on management’s margin guidance. Management continues to guide for non-GAAP product gross margin near 75% for the full fiscal year, even as short-term margin pressure persists from rising GPU costs tied to the company’s expanding AI initiatives.

The net revenue retention rate remains a key metric to monitor for Snowflake, as it shows how much existing customers are expanding their spending over time. The company most recently reported a 125% net revenue retention rate in fiscal Q2 2026, following 126% in fiscal Q4 2025, meaning customers, on average, are spending roughly 25% more than they did a year earlier. Sustaining retention at this level indicates continued expansion within the installed base, even as usage patterns normalize across the industry.

Operating margin expectations are critical, as Snowflake posted a -30% GAAP operating margin in fiscal Q2 2026 despite strong revenue growth, and many investors are looking for clearer operating leverage in the expense base, particularly improved sales and marketing efficiency, to support the stock’s premium valuation.

📅 Thursday, Dec 4th

- Kroger Company (KR): Kroger will report Q3 2025 financial results, with consensus expectations calling for $1.03 earnings per share and $34.25 billion in revenue, representing 8.4% year-over-year EPS growth and about 1% revenue growth respectively.

Identical sales growth excluding fuel remains an important indicator to watch, following Kroger’s 3.4% increase in the second quarter driven by pharmacy, fresh produce, and e-commerce. Management has guided that Q3 identical sales are expected to come in slightly below the midpoint of its full-year outlook of 2.7% to 3.4%. E-commerce sales growth is a key performance indicator to track, as Q2 delivered 16% year-over-year e-commerce growth with delivery surpassing pickup for the first time, showcasing Kroger’s omnichannel execution despite broader market share headwinds.

Finally, competitive positioning and market share trends remain a backdrop concern, as Kroger’s market share has declined from 9.8% to 8.5% over five years while Walmart and Costco have gained ground, requiring investors to assess whether management’s turnaround initiatives and strategic investments can stabilize or reverse this erosion while maintaining margin discipline.

We hope this helps and happy trading!

– Trade and Travel Team

Related Blogs

Follow Us

Testimonials

Hear from students on why they chose the Trade and Travel Family and how it has changed their lives.