Major U.S. equity indices closed lower last week amid renewed macroeconomic jitters. The S&P 500 (SPY) fell 2.54%, while the Nasdaq Composite (QQQ) dropped 2.35%, and the Dow Jones Industrial Average (DIA) declined 2.4%.

A key catalyst was Moody’s surprise one-notch downgrade of the U.S. credit rating from Aaa to Aa1, which rattled market participants. At the same time, President Trump’s renewed 50% tariff threat on European goods and a proposed 25% levy on non-U.S. iPhones stoked fresh trade-war fears, sparking another sell-off.

Looking ahead (with Monday’s Memorial Day market holiday), market participants will focus on key economic data and signals from the Fed. The Fed’s preferred inflation gauge, core PCE, is set to be released along with minutes from the central bank’s May meeting. Earnings from major companies, such as chipmakers and large retailers, may also influence sentiment in the shortened week. In this environment, traders will be watching whether U.S. growth and inflation data support the market’s optimism or keep investors cautious.

📅 Wednesday, May 28th

- FOMC Meeting Minutes: The FOMC Meeting Minutes from the May 6-7 meeting will provide detailed insights into the Fed’s decision to hold rates unchanged at 4.25%-4.50% for the third consecutive meeting. Market participants should closely examine any discussion about tariff impacts on inflation expectations, the timing of potential rate cuts (with markets currently pricing in 29% odds of a July cut), and how the committee views the balance between their dual mandate goals amid rising unemployment and inflation risks. Traders will particularly focus on any commentary regarding the Fed’s quantitative tightening pace of $5 billion in Treasury securities and $35 billion in mortgage-backed securities monthly, as well as individual members’ views on when economic data might warrant policy adjustments.

📅 Thursday, May 29th

- Prelim GDP q/q: The upcoming second estimate of U.S. GDP is expected to confirm the preliminary -0.3% quarterly contraction, marking the first economic decline since early 2022. Market participants should focus on revisions to key components, particularly whether the record 41.3% surge in imports that drove the initial decline gets adjusted (as businesses front-loaded purchases ahead of tariffs), along with any changes to the 1.8% consumer spending growth rate and the $140.1 billion inventory accumulation that partially offset the trade deficit impact. Traders will closely monitor whether the final numbers support the narrative that this contraction was primarily driven by tariff-induced stockpiling rather than underlying economic weakness, as any upward revisions could signal stronger domestic demand resilience and reduce recession fears that have pushed the probability to 35%.

- Unemployment Claims: The upcoming weekly initial jobless claims report is forecast to rise to 229,000 from the previous week’s reading of 227,000, representing a modest increase of 2,000 claims that would align with the recent trend of gradual labor market softening. Market participants and traders should closely monitor whether the actual reading exceeds the 229,000 forecast, as this could signal accelerating job losses, while also watching for any significant state-level variations like the recent surge in Massachusetts (+3,410) or declines in Michigan (-5,827) that have driven weekly volatility. Most critically, market participants should focus on continuing claims data, which recently climbed above the psychologically important 1.9 million threshold and sits at a four-week moving average of 1,873,500, as persistent elevation in this metric would indicate growing difficulty for unemployed workers to find new positions and could influence Federal Reserve policy expectations.

📅 Friday, May 30th

- Core PCE Price Index m/m: The upcoming Core PCE Price Index month-over-month report, forecasted to rise 0.1% compared to the previous reading of 0%, represents a key test for inflation momentum as the Federal Reserve closely monitors this preferred inflation gauge against its 2% annual target. With the annual Core PCE currently running at 2.6% in March 2025, above the Fed’s target, traders will scrutinize whether the monthly reading meets, exceeds, or falls short of the 0.1% forecast, as any deviation could significantly impact USD strength and interest rate expectations. Market participants should watch for immediate market reactions, as a higher-than-expected reading above 0.1% would likely strengthen the dollar and reduce expectations for Fed rate cuts, while a softer reading could weaken the USD and boost rate cut probabilities.

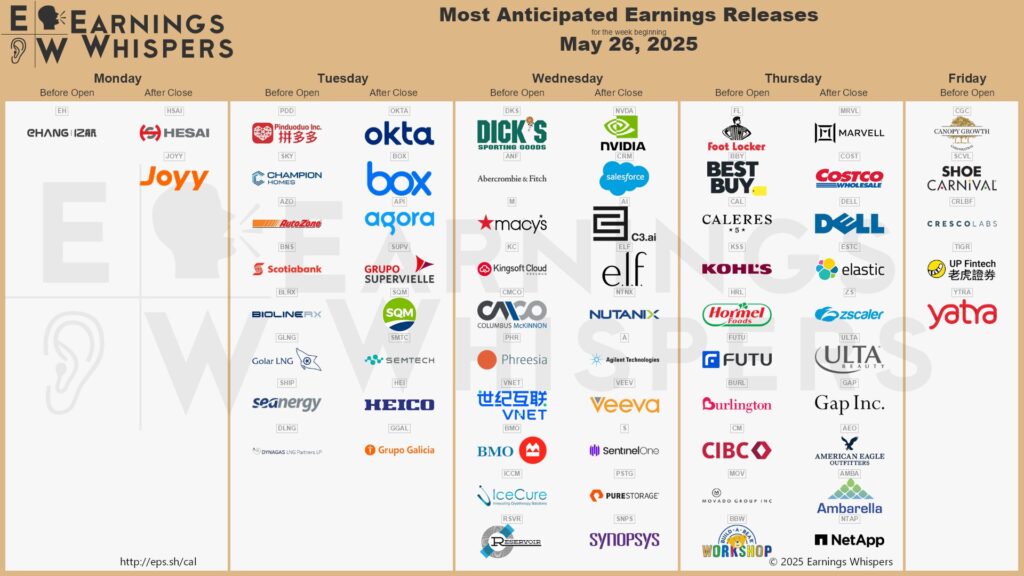

Q1 earnings season is drawing to a close. Here are some of the companies set to report this week:

📅 Tuesday, May 27th

- AutoZone, Inc. (AZO): AutoZone is set to report its earnings with analysts expecting EPS of $37.11 and revenue of $4.42 billion, representing modest growth of 1.1% and 4.2% year-over-year respectively. Market participants should closely monitor same-store sales growth (projected at 1.3%), the performance of the company’s domestic commercial business, which grew 7.3% in Q2, and progress on the mega hub expansion strategy as AutoZone works toward its goal of opening over 200 locations from the current 111. Given that AutoZone has missed earnings estimates in three of the past four quarters with an average negative surprise of 3.23%, traders will be particularly focused on whether the company can reverse this trend while navigating challenges from weather impacts and discretionary spending pressures.

📅 Wednesday, May 28th

- NVIDIA Corporation (NVDA): Nvidia will report its earnings with analysts expecting earnings of $0.74 per share on revenue of $43.30 billion, representing 21.3% and 66.2% year-over-year growth respectively, though results will include a significant $5.5 billion charge related to unsold H20 chip inventory due to U.S. export restrictions to China. Market participants should focus on data center revenue performance, gross margin trends (expected around 71%), and critically, the company’s Q2 guidance, which analysts project at approximately $46.51 billion in revenue, as supply constraints for Blackwell chips and the ongoing impact of China trade restrictions remain key uncertainties. Market participants should also watch for updates on Blackwell chip production ramp, AI demand sustainability, and management’s commentary on navigating geopolitical headwinds.

- Salesforce, Inc. (CRM): Salesforce is set to announce its earnings with analysts projecting adjusted EPS of $2.55 (up 4.5% year-over-year) and revenue of $9.75 billion, reflecting 6.7% growth from the prior-year period. Market participants should monitor current remaining performance obligation (CRPO) growth, which faces tougher comparisons at 10% year-over-year, and progress on AI-driven initiatives like Agentforce (3,000+ paid customers) and Data Cloud, which surpassed $900 million in annual recurring revenue last quarter. The report follows February’s disappointing FY26 revenue guidance of $40.5-$40.9 billion (7-8% growth), making execution against macroeconomic headwinds and elongated deal cycles critical for restoring confidence.

📅 Thursday, May 29th

- Costco Wholesale Corporation (COST): Costco is scheduled to report earnings with analysts expecting earnings per share of approximately $4.23-$4.25, representing a 11.98-12.43% year-over-year increase, and revenue of around $63.11 billion. Market participants should closely monitor the impact of the membership fee increase that took effect in September 2024 (raising Gold Star memberships from $60 to $65 and Executive memberships from $120 to $130), as this marks the first fee hike in seven years and affects approximately 52 million members. This quarter might show more normalized membership revenue uplift. Key metrics to watch include comparable sales growth trends (April showed 4.4% total company growth with strong 12.6% e-commerce growth), membership renewal rates, and gross margin expansion, particularly given the company’s recent strong performance with April net sales reaching $21.18 billion, up 7.0% year-over-year.

- Dell Technologies (DELL): Dell Technologies is scheduled to report its earnings with consensus estimates calling for adjusted EPS of approximately $1.71 and revenue between $23.17 billion, representing roughly 4.1% year-over-year growth. Market participants should focus on the Infrastructure Solutions Group’s performance, particularly AI server shipments which Dell projects will contribute over $15 billion in revenue for the full fiscal year 2026, as well as any updates on the company’s $9 billion AI server backlog and progress with major deals including the reported $5+ billion contract with xAI. Key margin metrics will be closely watched given Dell’s guidance for a 100 basis point decline in adjusted gross margin for FY26 due to higher AI server production costs, while the Client Solutions Group’s PC business remains under pressure from weak consumer demand.

We hope this helps and happy trading!

– Trade and Travel Team

Related Blogs

Follow Us

Testimonials

Hear from students on why they chose the Trade and Travel Family and how it has changed their lives.